2020 was unforgettable, especially for Bitcoin. To help memorialize this year for our readers, we asked our network of contributors to reflect on Bitcoin’s price action, technological development, community growth and more in 2020, and to reflect on what all of this might mean for 2021. These writers responded with a collection of thoughtful and thought-provoking articles. Click here to read all of the stories from our End Of Year 2020 Series.

A “biblical flood of liquidity” was released onto the world this year by its largest central banks, raising fears for the longevity of several of the world’s currencies. In reviewing the major monetary policy changes from the Federal Reserve, the European Central Bank and the Bank of Japan, it’s clear that 2020 was an unprecedented year for the legacy economy and that there is strong need for an alternative that is free of inflation and middlemen.

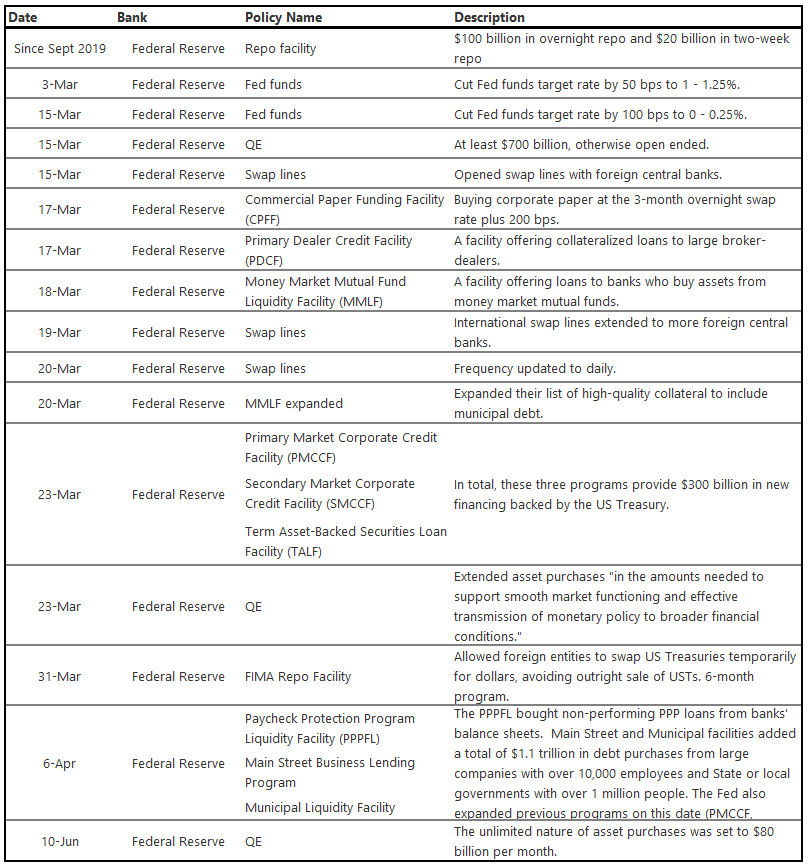

The Federal Reserve

- Decreased its funds target rate by 150 basis points (bps) to 0 percent

- Started open-ended quantitative easing (QE) of $80 billion per month

- Provided a potential $1.95 trillion in lending in many different programs

- Extended $400 billion at the peak in currency swap lines with foreign central banks

While the Federal Reserve’s monetary response was the largest in absolute terms and most comprehensive of the major central banks, it was not the largest in relative terms.

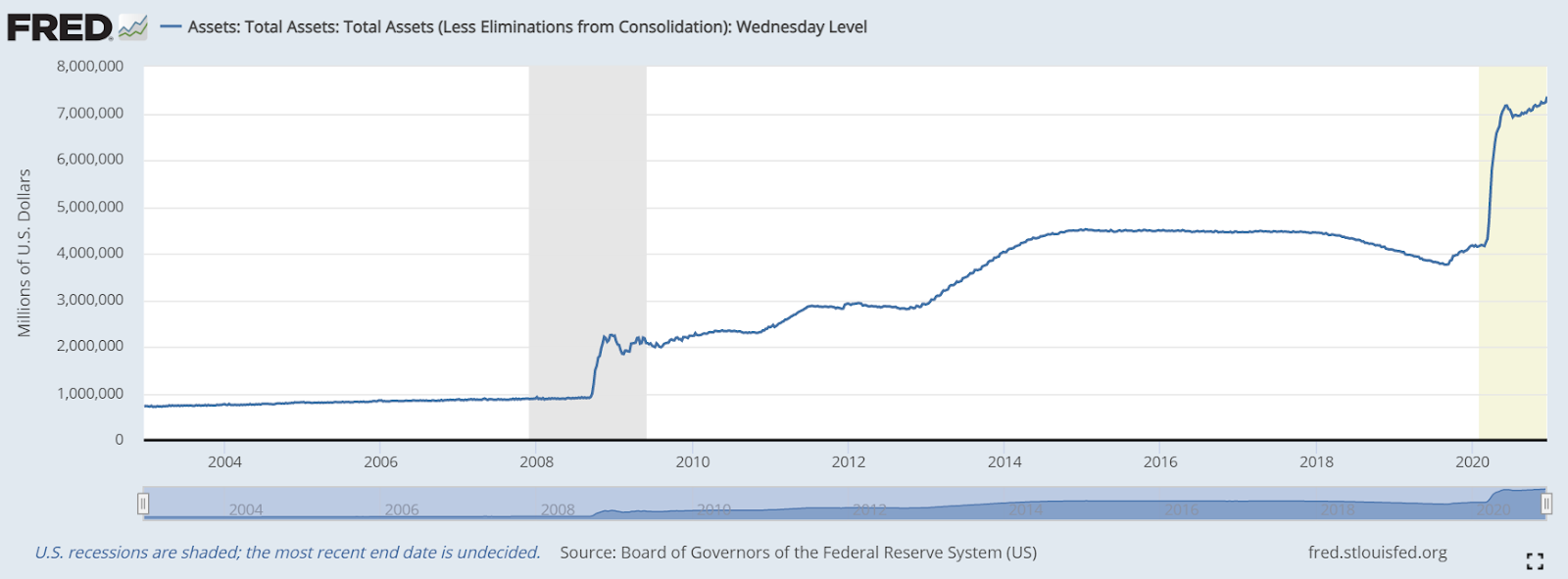

Cracks started appearing in the global financial system in 2018 with a slowdown in China, and the slowdown came to a head in September 2019 when repo rates spiked from near zero to 10 percent in the matter of one morning. This series of events set the Fed on a path toward “easier” monetary policy in 2019, with its balance sheet bottoming in Q3 and rising when entering 2020.

When the COVID-19 virus made the leap to Europe and then the U.S. in March 2020, it took the PhD economists by surprise. All major central banks responded between Sunday, March 15 and Wednesday, March 18 when it became obvious that the financial system was on the verge of collapse.

The response from the Fed was unique at first, since its baseline policy rate was above zero at 1.5 percent. In addition to that, it added what had become the typical monetary weapon by this point, large scale asset purchases (QE), followed by a new policy from Japan of buying corporate debt. Finally, it introduced several dizzying acronym programs in coordination with the U.S. Department of the Treasury to extend loans more broadly in the economy.

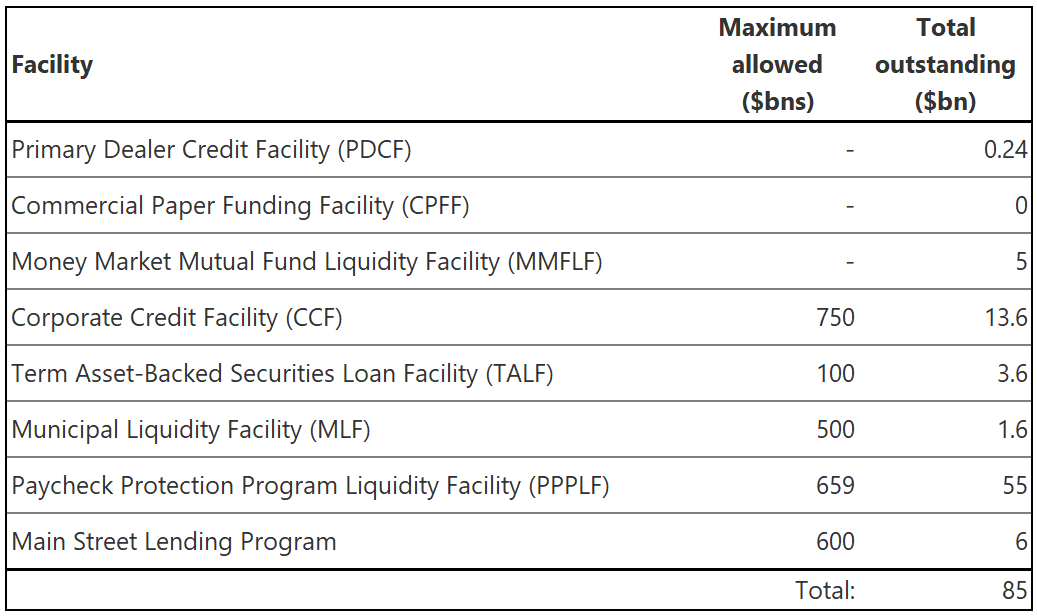

Though these new programs received a lot of attention in the press, they never got close to the maximum allowed levels and today stand almost unused. By April, all of the major pieces of the Fed’s response were in place and didn’t change much of anything, other than some reporting requirements in the second half of the year.

Federal Reserve Facility Balances

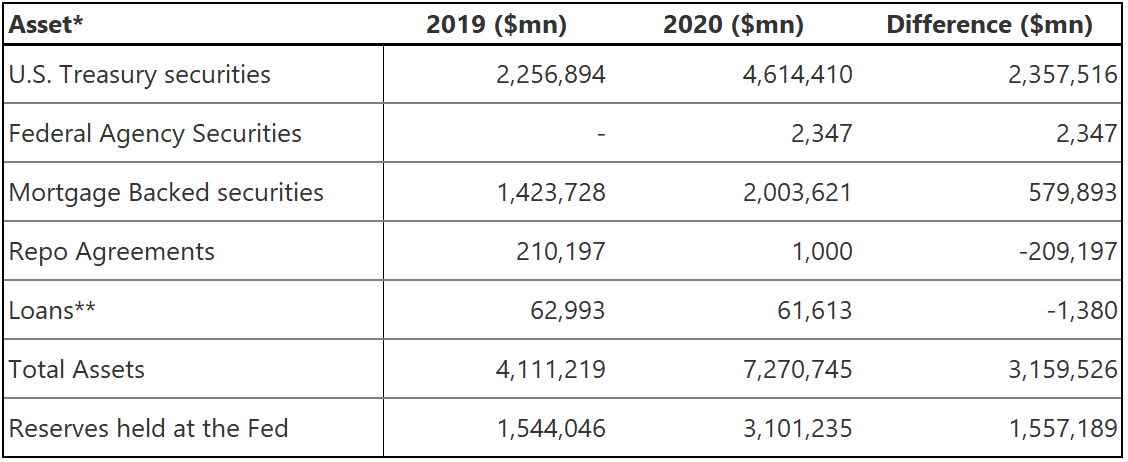

Federal Reserve 2020 Balance Sheet Changes

** Consists of many types of loans, including Facilities, listed above

European Central Bank

- Started 2020 already engaged in QE

- Gradually increased its one asset purchase program, the Pandemic Emergency Purchase Programme (PEPP), to €1.85 trillion

The European Central Bank’s (ECB) monetary policy this year was much more straightforward than the Fed’s. It has suffered from multiple financial crises since 2009 and was still in the midst of a QE program called the Asset Purchase Programme (APP), weighing in at €20 billion per month. That program did not change throughout 2020, but the PEPP was added to it. The PEPP eventually was extended to a total of €1.85 trillion in asset purchases to run through March 2022.

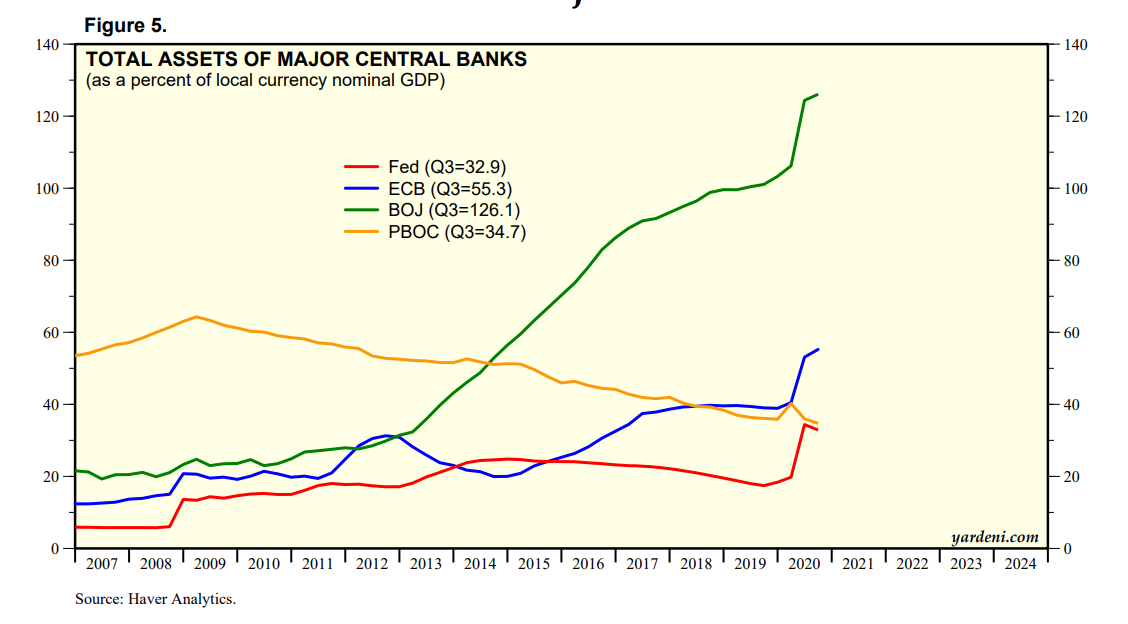

The ECB’s balance sheet soared to 55 percent of GDP in November, making the U.S. look tame in comparison at 34 percent and Japan look like the monetary basket case it is at 126 percent. Unless central bank monetary policy has nothing to do with inflation/deflation, if any country is going to experience inflation, one would assume it would be Japan, followed by the eurozone.

The European Central Bank managed to have the most simple policy on paper and it was implemented quickly, but it came back and increased it twice, with the most recent just this month.

The ECB has extended its intervention until March 2022, but it’s unlikely Europe can ever stop QE. At this rate, its balance-sheet-to-GDP ratio will reach 100 percent by the end of 2021.

* In addition to PEPP, multiple minor policy and rule changes came from the ECB this year, which can be found in the monetary policy press releases on the ECB’s website.

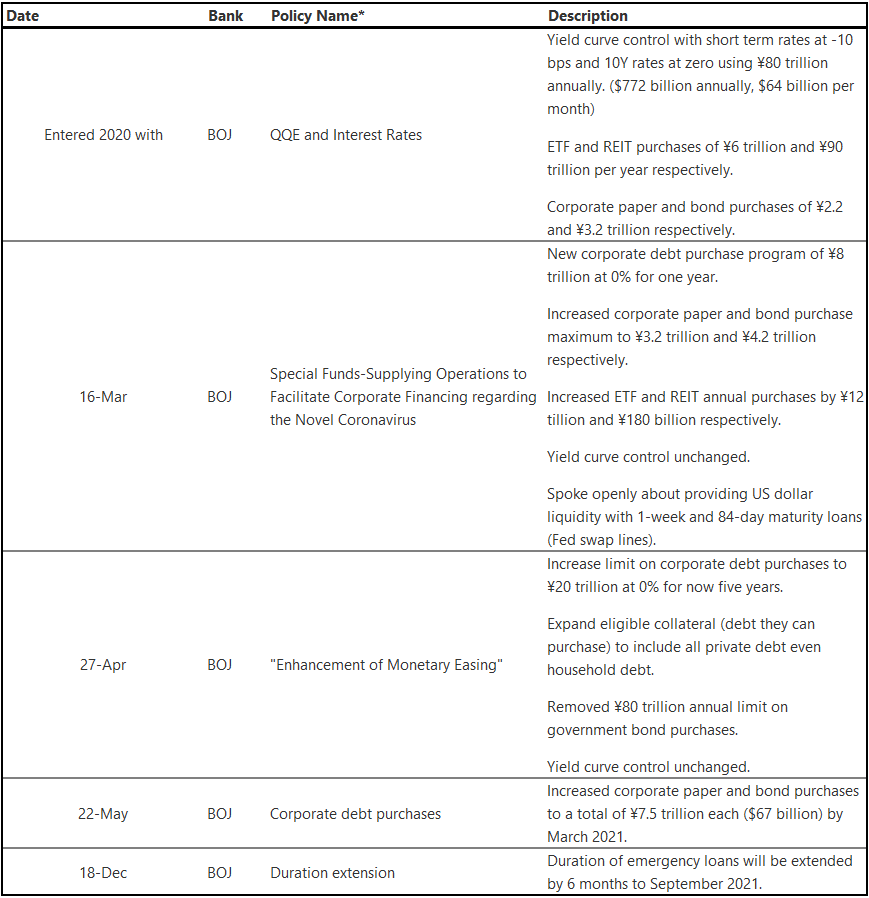

The Bank of Japan

- World’s longest running QE program

- Started the year already engaged in quantitative and qualitative monetary easing (QQE), consisting of broad spectrum purchases

- Took limits off government bond purchases and increased its already heavy market intervention

Lastly, the Japanese monetary policy is far in advance of anything the Fed or the ECB are doing, and 2020 was no exception. In 2013, Japan embarked on QQE, where it not only purchased government and agency bonds, but also directly bought other securities like ETFs and Japanese REITs.

The Japanese began this modern era of QE almost 20 years ago, and in 2020, with all of the central banks uniformly walking down the same path it did with asset purchases, Japan says, “hold my beer.” It is in a truly scary monetary and demographic crisis with no obvious escape.

Its interventions for 2020 are well over $1 trillion dollar equivalent for a GDP of less than $5 trillion (more than 20 percent). Compare this to the eurozone rate of nearly $2 trillion in stimulus for a $18 trillion economy (11 percent), or the U.S. with $3 trillion for a $20 trillion economy (15 percent).

Central Bank Balance Sheets Relative To GDP

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The post Reviewing 2020’s Central Bank Policies appeared first on Bitcoin Magazine.

via bitcoinmagazine.com