Announced today, Tether, the leading stablecoin issuer, has emerged with a robust balance sheet showcasing ownership of over $2.8 billion in Bitcoin. The information comes to light following an audit conducted by BDO, a renowned auditing firm, as detailed in the official auditor's report.

The audited report provides a comprehensive analysis of Tether's financial standing, including more information on its Bitcoin holdings. Tether, known for its stablecoin USDT, has consistently played a massive role in the cryptocurrency market, facilitating transactions and maintaining a peg to the US Dollar.

"At Tether, we look forward to great 2024, with many new projects and products ready to come alive," said Tether CEO Paolo Ardoino. "I'm really excited by Tether's expansion. While Tether is mostly known for one product (USDT), the company is becoming an investor and infrastructure builder in many strategical sectors, spacing from AI to P2P telecommunications, from Bitcoin mining to renewable energy production."

The company also had a $2.85 billion profit for last quarter, of which about $1.85 billion came from gold and bitcoin holdings. For all of 2023, Tether achieved a profit of $6.2 billion.

So, 2023 has been pretty epic for Bitcoin. It's like Bitcoin woke up and decided to flex its muscles big time. We're talking a massive leap, over 140% in value – that's huge! It's not just about topping traditional rivals like gold; it's also about leaving other cryptocurrencies in the rearview mirror. Let’s dive into the on-chain action and the exchange buzz, trying to piece together clues to see what Bitcoin might be up to in the coming year.

Bitcoin's Blast from the Past

According to Glassnode's report, we’re seeing a déjà vu with Bitcoin cycles in 2015-2017 and 2018-2022 in terms of how long it's taking to bounce back and the drawdown since the all-time high (ATH).

Source: Glassnode

In the current cycle, Bitcoin has seen a drawdown of about -37% from its ATH, which is pretty close to the -42% in 2013-2017 and -39% in 2017-2021. Plus, since the FTX lows in November 2022, Bitcoin prices are up a solid +140%, making it the strongest one-year return compared to the +119% in 2015-2018 and +128% in 2018-2022.

Exchange Activity: Bitcoin's Trading Paradox

Despite 2023 being a banner year for Bitcoin, the number of transactions depositing funds to exchanges has surprisingly hit multi-year lows. But here's the kicker: Glassnode data shows that the on-chain volume flowing in and out of exchanges has skyrocketed, jumping from $930 million to a staggering $3 billion – that's a massive 220% increase.

This discrepancy between fewer deposits yet skyrocketing volume makes us wonder: what's driving the intensified exchange activity if not retail investors? On one hand, the decrease in deposit transactions might suggest that investors are becoming more cautious about leaving their assets on exchanges, possibly due to security concerns or a desire for greater control over their funds. This is where the potential shift towards non-custodial exchanges like StealthEX comes into play. Given the FTX drama that's still on everyone's mind, it's no surprise that these platforms where you can keep your private keys are becoming more popular.

There's a serious uptick in on-chain volume showing that trading and speculation are buzzing more than ever. It seems that while investors might be shying away from depositing their funds, they are actively trading and moving large sums of money. This could be a sign of growing institutional interest, especially as we see the average size of deposits to exchanges nearing the previous all-time high of $30k per deposit, according to Glassnode.

Moreover, the fact that exchange deposits as a percentage of all transactions have dropped from around 26% in May to just 10% today, yet the decline is more modest (around 20%) when adjusted for Inscriptions, adds another layer to this narrative. Undeniably, we're witnessing a dynamic shift in the blockchain sphere as novel transaction types emerge and new players grab their share of the limelight.

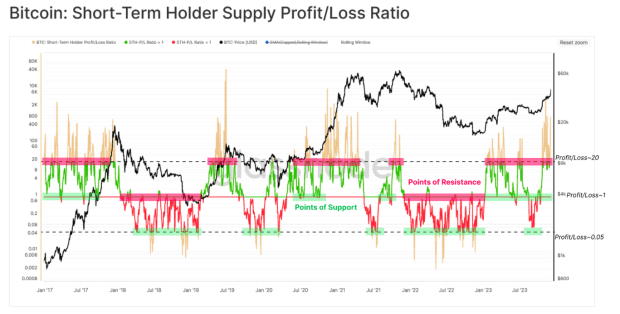

Short-Term Holders Cashing In

Short-Term Holders (STHs) have been making some smart moves lately, cashing in on their Bitcoin investments at just the right time. Glassnode's got the stats to prove it – the STH-Supply Profit/Loss Ratio has been hovering above ~1 since January. This means these savvy traders have been playing the 'buy-the-dip' game pretty well, a classic move in uptrends. However, these STHs are moving hefty amounts of coins to exchanges, and the gap between what they paid and what they're selling for is pretty sizable.

Source: Glassnode

The first week of December, when Bitcoin hit $44.2k, STHs jumped into action, seizing the moment to take profits. It's like they saw the wave coming and rode it all the way to the shore, capitalizing on the demand liquidity. This activity has put a bit of a pause on Bitcoin's upward climb, demonstrating STHs’ sway over crypto prices.

Wrapping It Up: Bitcoin and Beyond

So, there you have it – Bitcoin's 2023 story is a mix of triumphs, challenges, and a whole lot of excitement. Bitcoin, in its digital universe, never fails to keep us intrigued with its roller-coaster ride of strong recoveries and declines that resonate with historical patterns, even bouncing back recently despite a few bumps on the road. The play of STHs and the unpredictable ebbs and flows of exchange activities knit together a complex, yet intriguing narrative. Regardless of whether you're in it for the highs or the lows, or simply out of sheer curiosity, observing Bitcoin's ride is undoubtedly one to watch.

This is a guest post by Maria Carola. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

In Texas, the legacy of mineral rights ownership is a narrative etched into the very bedrock of state history. Passed down through generations like a cherished heirloom, the ownership of mineral rights is more than a legal claim; it is a cultural emblem, a symbol of resilience, and a precious legacy. The wealth and prosperity created for mineral rights owners in Texas over time through the extraction and production of hydrocarbon minerals is tremendous but also comes with a heavy responsibility. That responsibility demands a farsighted financial perspective and a commitment to ethical and environmental stewardship to ensure the well-being of future generations who will inherit the mineral estate. It is common knowledge among native Texans that nothing should ever be done to jeopardize their ownership rights. “Never sell your mineral rights” is a commonly heard expression for Texas natives.

The reason generations of Texans have kept their mineral rights intact within their families is that the modern global economy rests almost entirely upon the benefits of the extraction, refining, and processing of these subsurface minerals. When you own mineral rights, you own the fundamental primary material that allows the production and distribution of nearly all of the goods and services our civilization enjoys. In the future, the world’s economic production will similarly rely on Bitcoin to coordinate large transactions between manufacturers and industrial firms.

Texas Mineral Rights

Mineral rights represent ownership of subsurface materials and the right to sell, develop, and produce those materials. Texans have been fortunate to have the right to access the valuable mineral and hydrocarbon reserves located beneath their properties for more than 150 years. Mineral owners can track ownership through legal records dating back to the 1866 state constitution of Texas, which was formed to meet the requirements to reenter the United States after seceding five years earlier and which firmly established privately held mineral rights.

It is essential to understand that mineral rights in Texas can, and predominantly are at this point, severed from the rights of ownership of the land surface. These two distinct property rights are often referred to as the mineral estate and the surface estate. In addition to the ability to separate the mineral estate from the surface estate, the mineral estate can be subdivided into fractional shares of ownership. In Texas, it is commonplace for mineral estates to be divided into tiny fractional ownership shares. Whether the same owner holds the mineral ownership and surface ownership or they have been separated sometime in the past, according to Texas law, the mineral estate holds a position of supremacy over the surface estate. This authority allows the mineral rights owner to use the land's surface to explore, develop, and produce oil and gas under the property. The mineral rights holder usually accomplishes this by entering into a contract (mineral lease agreement) with a specialized company to explore and extract resources from the property in exchange for a lump sum payment followed by ongoing royalty payments that result from selling the resources to the market.

4 Pillars Of Modern Society

The standard of living in our modern society would not be possible without the massive widespread use of fossil fuels extracted from below the earth’s surface. In his book “How the World Really Works,” author Vaclav Smil masterfully explores our total dependence on fossil fuels to provide four indispensable materials our civilization relies upon. These fundamentally essential materials are cement, steel, plastics, and ammonia.

Approximately 17% of the world’s energy supply is needed to produce these four critical materials. Your ability to use the internet and every connected device ultimately depends on fossil fuel hydrocarbons. The infrastructure and technologies of the modern world are only possible through their use, and they are the sole means to provide food for 4 billion people. In his book, Smil explains the crucial role each of these materials plays in the function of our global economy. Their production heavily relies on fossil fuels with no other viable energy substitutes. Smil reports that the global annual production of cement is 4.5 billion tons, steel is 1.8 billion tons, plastics are nearly 400 million tons, and ammonia is 180 million tons.

Currently, there are no feasible alternatives to using steel or cement to construct the world's infrastructure. Their combination of strength, durability, and adaptability is unmatched by any other materials. The production of cement and steel requires intense heat, which is currently only possible by way of the combustion of fossil fuels. Replacing the aging infrastructure of developed countries and building new infrastructure in underdeveloped nations will require continual vast amounts of new cement and steel production.

Not only do ammonia and plastics require a large amount of energy in production, but they also are formed using hydrocarbon-derived inputs. 50% of worldwide food production relies on ammonia fertilizer, produced using hydrogen that is sourced from natural gas. Natural gas is also the energy source that provides the high pressure and temperatures required for the process.

Over 99% of plastics are derived from the refining of fossil fuel hydrocarbons. No alternative material offers the same extensive benefits of plastic’s light weight, flexibility, durability, and usefulness. The world enjoys countless products that contain plastics, such as automobile and appliance parts, consumer electronics, food packaging, furniture, and life-saving medical equipment found in hospitals. Petroleum refining also provides critical elements such as adhesives, engine lubricants, detergents, coolants, inks, pharmaceuticals, coatings, and textiles.

Eliminating fossil fuels from the global energy supply in the next few decades is an unrealistic goal when we honestly consider the available data. Due to our physical and real-world constraints, the transition to a decarbonized, renewable energy-driven economy poses a nearly insurmountable challenge.

Hydrocarbon minerals play a prominent role in the beginning stages of mass-scale modern production, and the transport of final goods depends almost entirely on hydrocarbon fuels. Tracing the stages of production processes backward from the final stage of consumer goods and services to the original input of fossil fuel hydrocarbons, we find that the ownership of mineral rights at the first stage of production signifies a pivotal position of influence over the economic landscape. This position grants mineral rights owners the immense power to shape and dictate economic destiny for every individual, business, and nation. Our global economy rests upon mineral rights owners' discretion to allow their property to be utilized.

Just as owning mineral rights is owning the base material that underpins the functioning of the entire global economy, owning bitcoin today is owning the mineral rights to the future economy. The worldwide economy will one day function through the exchange of bitcoin between productive entities. Those who own bitcoin will own the financial collateral that allows the economy to function and transact.

Bitcoin And Mineral Rights

Bitcoin and mineral rights may seem like disparate concepts, but share some similarities. Both are subject to the concept of limited supply. In the case of Bitcoin, there will only ever be 21 million coins in existence due to its programmed scarcity. Similarly, mineral rights pertain to owning scarce mineral resources found underground. Both Bitcoin and mineral rights have forms of ownership, meaning both can be bought, sold, or transferred to others. The value of each asset is determined by market demand and supply dynamics, and each has experienced significant price fluctuations over time. Both mineral rights and Bitcoin share the feature of being decentralized. Bitcoin operates on a decentralized network, with no single entity controlling its issuance or transactions. Likewise, mineral rights represent ownership of an asset found across the globe without a centralized issuer. Each asset also has a substantial cost to its extraction and release into the arena of human economic activity. Oil and gas extraction from underground requires significant investments of financial capital, labor, and energy. Generating new supply in the Bitcoin network also requires considerable energy expenditures and capital investments in physical hardware and infrastructure.

The scarcity of bitcoin derives from its programmed 21 million supply cap, but bitcoin scarcity also develops because of its relative relationship with the entirety of the world’s goods and services. As the nominal amount of goods and services grows at a rate higher than the rate of supply of new bitcoin, bitcoin becomes more scarce relative to these goods and services because it grows more slowly. This relative aspect of Bitcoin to our economy creates a second layer of scarcity beyond the programmed supply limit of 21 million. As this second layer of scarcity grows over time due to the network effects of an expanding economy, other forms of storing value become perpetually inferior to this better store of value.

The price of everything in terms of bitcoin is always trending downward, making it a better way to preserve capital than other forms. For example, new industrial building construction costs have increased by 46% in the past five years, meaning an industrial capital project that cost $100 million five years ago might cost $146 million today. However, when priced in Bitcoin terms, the cost for this project has reduced by nearly 90%, from 26,253 BTC five years ago to 3,395 BTC today. As the world continues to become more productive, the value of those productivity gains is stored in the most dominant store of value. That store of value is Bitcoin, and as global market participants increasingly understand this, the value of Bitcoin will trend upward forever.

Within the domain of current Bitcoin commentary, it is common to hear or read about a future where merchants will sell their goods in exchange for payment by Bitcoin or other related applications functioning on top of the Bitcoin network. Retail merchant adoption will undoubtedly help build Bitcoin demand and incrementally enlarge the network’s value. However, the most considerable impact on the growth of bitcoin demand will arrive when the owners of the world’s factors of production begin to demand bitcoin as payment for their goods.

Bitcoin And Production

Firms participating in the various stages of productive processes will start to understand the economic phenomenon of holding cash balances that increase in value while simply holding them, and therefore, will begin to demand bitcoin. Cash balances that accrete value instead of declining in value over time simplify financial planning for large capital expenditures. Significant capital investments in new projects become more manageable to facilitate. Businesses can finance capital projects more efficiently using their cash reserves held in Bitcoin rather than relying on debt or equity financing that dilutes shareholder value. Financial officers managing a company's capital structure will break into a new era of corporate finance when they begin calculating the net present value of an investment made with money that appreciates in value over time instead of depreciating.

When a firm chooses to invest in productive endeavors, the firm does so in anticipation of earning a resulting return of greater value. When a company uses accumulated Bitcoin to fund a capital project, it will consequently only accept Bitcoin as a return on investment. Accepting an inferior form of money in return will be unacceptable. As manufacturing and production businesses increasingly adopt Bitcoin as a medium for coordinating exchanges of value in manufacturing processes, the Bitcoin network will absorb significant amounts of value from the existing monetary system. This process will create a circular exchange, strengthening Bitcoin's store of value characteristic and increasing demand among companies supplying production factors throughout supply chains.

When the use of Bitcoin to facilitate large value exchanges between businesses becomes widespread, the availability of Bitcoin in the market will become limited. At that point, the only way to acquire Bitcoin will be by providing something of value in return. Purchasing Bitcoin with other forms of currency from a money exchange will become rare, and those who wish to obtain Bitcoin will instead have to earn it. Bitcoin will become all but unavailable for purchase through traditional means.

There will be a day when the producers of capital-intensive goods and scarce natural resources stop accepting continually and purposefully diluted money for their products. In the future, when large payments of value between manufacturers and industrial firms are made through Bitcoin, the worldwide economy will become dependent on it to function. Those who have accumulated bitcoin in advance of this will find themselves in a position of dominance. Just as the owners of subsurface mineral rights today profit by allowing their property to be utilized to power the global economy, bitcoin owners will one day profit by administering the money that coordinates worldwide economic production.

Owning Bitcoin today is owning the mineral rights to the future.

This is a guest post by Aaron Roberts. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine's premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Last week, I put the massive buying pressure coming to bitcoin in context, but there is another — perhaps the largest — source of potential demand entering the scene.

We already know the Bitcoin ETFs, MicroStrategy issuing more shares to buy more bitcoin, Tether’s constant buying, and the halving will all be major sources of demand this cycle. For example, in the first two weeks of trading alone, the “newborn 9” accumulated 125,000 BTC. That has, so far, been offset by GBTC outflows, but it is unlikely that all GBTC holders are captive sellers who will get out ASAP. This outflow should start to wane in the coming weeks.

A somewhat unexpected development is emerging in China of all places. Readers of my content here and on bitcoinandmarkets.com won’t be strangers to what’s happening in China over the past couple of years. They are experiencing the end-of-an-economic-model transition. The China we have grown to know was built on debt, producing goods for over-indebted foreign customers. They are heavily dependent on globalization and a highly elastic monetary environment. That era is coming to an end, and the crash of the Chinese real estate market, and now their stock market, are visible signs of the end of that paradigm.

On January 24, China Asset Management Company (China AMC), a gigantic fund manager and ETF provider in China, halted trading on their Nasdaq 100 and S&P 500 ETFs to stop the flood of money out of other funds and into these US-connected funds. On Tuesday, other US-connected ETFs on Chinese markets opened limit up, and had a 21% premium over NAV. The flight to safety is also affecting Chinese-based Japanese ETFs. Tuesday saw the China AMC’s Nomura Nikkei 225 ETF rise over 6% to a 22% premium.

Chinese investors are in full-on panic mode, and the authorities are barring the door. It is only a matter of time until more Chinese investors start tapping bitcoin for its store-of-value and portability. Many Chinese are already familiar with bitcoin. China used to be a dominant source of demand for bitcoin until the CCP banned it in 2021.

While bitcoin is still officially banned in Mainland China, investors can still use exchanges like Binance and OKX. They can also buy OTC, person-to-person, or via off-shore bank accounts. Last year, Hong Kong very publicly opened back up to bitcoin. They have been following in lockstep behind US regulators giving Bitcoin the official blessing in Hong Kong. It is unlikely that Hong Kong authorities would make such a public push for legalizing bitcoin only to turn around the next year to ban it.

This morning, a piece from Reuters quotes a senior executive of a Hong Kong-based bitcoin exchange, who confirms this capital flight story. “Investment on the mainland [is] risky, uncertain and disappointing, so people are looking to allocate assets offshore. [...] Almost everyday, we see mainland investors coming into this market.”

The source added, “If you are a Chinese brokerage, facing a sluggish stock market, weak demand for IPOs, and shrinkage in other businesses, you need a growth story to tell your shareholders and the board.”

We have been talking about Bitcoin providing a parallel world of green shoots, and now it is being recognized everywhere.

The flows from China will be a big source of demand in this cycle, and the approval of bitcoin spot ETFs in the US will create a perfect synergy via allowing sophisticated foreign investors to buy bitcoin and US-based assets at the same time.

We cannot forget about the faltering European markets either. Europe is likely already in recession. By December, EU factory activity had contracted for 18 straight months. Germany barely avoided a technical recession despite 2023 GDP being negative at -0.2%. The relative attractiveness of bitcoin is very high in a world of capital flight and negative growth. Many bitcoiners are worried about a recession bringing a stock market crash, which would force selling of bitcoin like it did in March 2020, but it might be the opposite this time around. As investors realize that the old system is stagnant and decaying, Bitcoin’s unique convergence of properties as revolutionary tech, a fixed supply asset, and economic growth potential will be where capital flees into.

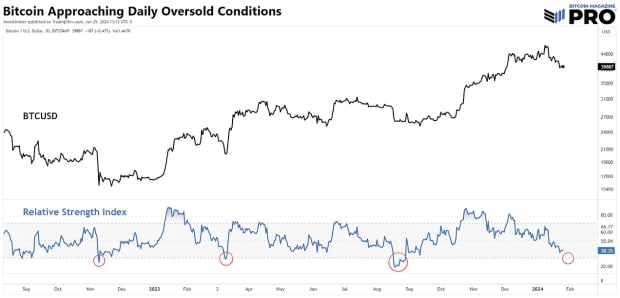

Bitcoin Price Update

Bitcoin’s price performance has been disappointing since the ETF launch. However, in the context of FTX receivership selling $1 billion worth of GBTC and other large entities selling GBTC to rotate into lower capital fees of the new ETFs, price has held up extremely well.

RSI is one of the most widely used indicators and, as such, has a Schelling point effect. People and bots are watching for the daily RSI to hit oversold. Therefore, it is likely we won’t see any significant upside in price until 30 on the RSI is broken. That can be achieved by one more sell-off into support, since we are so close to 30 already. A more unlikely possibility is we could form a hidden bullish divergence, where the price makes slightly higher lows, but the RSI makes lower lows. I do not expect any significant downside either with the confluence of demand described above:we are at a temporary stalemate.

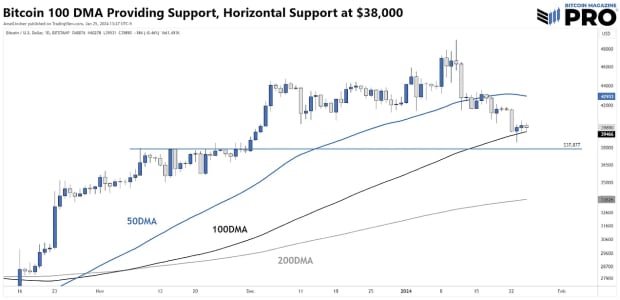

Staying on the daily chart below but zooming in, we see the 100 DMA is providing support currently. I also am watching the $37,877 level; an important price from back in November. Any dip that pushes RSI to oversold might not close below that.

The 100-day typically does not provide much support in bitcoin, with the 50- and 200-day moving averages being the most influential. However, below I show September 2020, right before the monster bull rally to end that year. The 100-day was the star back then. It is possible to hold along the 100-day and then rally with a pause in GBTC selling. Another interesting note from that period in 2020: the RSI stopped shy of oversold, catching many off guard as it shot to the moon. That is not my base case, but it does have precedence.

Bottom line, we are seeing massive and new sources of demand for bitcoin from the ETFs and now China capital flight. The ETF launch dynamics have been complicated but price has been relatively steady all things considered. It is only a matter of time until demand becomes apparent in price.

(NASHVILLE, TN – January 30th, 2024) Bitcoin Magazine, in collaboration with Kraken Digital Asset Exchange, is excited to unveil the 2024 Bitcoin Halving Livestream. This celebration, akin to a New Year's Eve variety show and featuring bitcoin’s biggest names, is dedicated to marking the fourth epoch in Bitcoin's history. Broadcasting live from Nashville, Tennessee, the event starts with the 839,979th Bitcoin block, with projections pointing to April 18, 2024, culminating in the milestone 840,000th block.

Mike Germano, President at Bitcoin Magazine, expresses his enthusiasm, "We at Bitcoin Magazine are thrilled to present the 2024 Bitcoin Halving Livestream in partnership with Kraken. This event is not just a celebration of Bitcoin's fourth epoch but a testament to the unyielding spirit of the Bitcoin community. It's an honor to mark this historic occasion, reflecting on our journey and looking forward to the boundless future of Bitcoin."

The event, a quadrennial tribute to Bitcoin’s growth and its distinctive culture, invites the community to witness the Top 21 Moments of the epoch, engage with Bitcoin advocates at the Bitcoin Halving LIVE Desk, and enjoy live coverage of global halving celebrations.The timing of the event, kickstarting at Bitcoin Block Height 839,979, adds an intriguing unpredictability. Additionally, the livestream will announce the winners of the Bitcoin Halving Challenge, sponsored by Nitrobetting, awarding a 1 BTC prize pool. Ledger, as the Official Mempool Sponsor, will visualize the Bitcoin network in real-time at bitcoinhalving.com.

“Kraken is thrilled to partner with Bitcoin Magazine for the upcoming Bitcoin halving. As two companies that have been industry leaders in driving Bitcoin awareness and adoption since the first halving back in 2012, it was only right to collaborate in bringing to light some of the most memorable moments of the last epoch and power the insightful conversations to come around this next historic halving,” said Lou Frangella, Director of Brand Partnerships for Kraken. “Our Mission to accelerate the adoption of crypto worldwide and that continues to be at the forefront of everything we do.”

The 2024 Bitcoin Halving Livestream, powered by Kraken, is set to be a landmark event in Bitcoin's history. Join Bitcoin enthusiasts around the world in this celebration of Bitcoin’s past, present, and future. Visit BitcoinHalving.com for updates and be part of this historic event by voting for the epoch’s Top 21 Moments, participating in the Bitcoin price prediction challenge competition, and tuning in to the livestream at the next Bitcoin halving.

About Bitcoin Magazine:

Bitcoin Magazine, the world’s first publication covering Bitcoin, serves its international readership with innovative ideas, breaking news, and global impact at the intersection of finance, technology, and Bitcoin. Operating from Nashville, Tennessee, Bitcoin Magazine is published by BTC Media. For the latest in Bitcoin news, visit BitcoinMagazine.com.

About Kraken:

Kraken is one of the world’s longest-standing and most secure digital asset exchanges, and is on a mission to empower people with new ways to connect and transact. Globally, Kraken clients trade more than 200 digital assets and 6 different fiat currencies, including GBP, EUR, USD, CAD, CHF and AUD.

Kraken was founded in 2011 and was one of the first exchanges to offer spot trading with margin, parachain auctions, staking, regulated derivatives and index services. Trusted by over 11 million traders and institutions around the world, Kraken offers professional, 24/7/365 customer support and one of the fastest, most performant trading platforms available. Kraken was the first company to conduct a Proof of Reserves audit and has committed to undergoing these audits on a regular basis.

Anarchy is a very dividing word to many people, inherently drawing the idea into peoples’ heads of complete and unbridled chaos. This is not on any level what Anarchy means. It is simply a system lacking rulers or a central authority, where all cooperation and coordination is done on a purely voluntary basis between peers in the system. The etymology of the original Greek word, anarhkia, itself literally just means “without rulers.” An, meaning without, arkhia, meaning rulers.

This concept is the foundational reality of why Bitcoin functions as a distributed network and protocol. There is literally no one in charge of the network. If there were, then it would not be a distributed system composed of sovereign individuals voluntarily choosing to interact with each other.

People tend to look at Bitcoin as some objective truth that functions as a frame of reference for human beings, that it exists in the same sense as the laws of physics. That is not true. This notion confuses the borders between objectivity, intersubjectivity, and subjectivity.

An objective truth is one that exists regardless of peoples’ subjective belief in it. I.e. The laws of gravity mean that an object with enough mass will exert its gravitational influence over all other objects around it. No amount of refusal to believe in this fact of the universe will change it. You can convince the entire human race to the last man, woman, and child, that the laws of gravity in fact do not exist. This will not stop gravity from exerting its influence on all of them.

Now take for instance the value of the dollar. Is the dollar inherently valuable? Is that an objective statement of truth? It is not. The only reason the dollar has value to any individual is because they subjectively value it. Why does an individual subjectively value the dollar? Because other individuals also subjectively value the dollar. This is intersubjectivity.

It is simply a subjective viewpoint shared amongst a large number of individuals. That is what Bitcoin is, a distributed intersubjective system. So what is the difference between Bitcoin and the dollar? The lack of rulers and coercion. The dollar system has people in charge of it, the Federal Reserve, the commercial banks that actually issue new dollars by offering credit, the government agencies that regulate its use and who can interact with it. It has tax authorities mandating its use in the payment of your tax obligations.

Bitcoin has no such equivalent rulers. It has no Federal Reserve board, it has no commercial banks that dictate when and in what quantities dollars are brought into circulation. It has no taxes that you are coerced into paying by anyone. It is simply a distributed set of economic actors voluntarily running a piece of code in order to interact with each other.

“But Bitcoin has rules.” Yes, it does. That people voluntarily opt into. There is no power structure or governance structure involved in creating those rules. They were put out into the world by Satoshi Nakamoto, and every single person who has joined the network since that moment in time freely chose to adopt those rules. There is no structure saying “these are the rules.” There is simply the set of rules that everyone has voluntarily chosen to follow completely of their own accord.

Even changes to those rules that have occurred over the years, and there are quite a few of them, are purely voluntary in their nature. There was no governance structure or authority that imposed them on anyone. There are no “rules to change the rules.” Anyone at any time can step up into the social square and propose a new rule to add to the Bitcoin protocol and network. At any time people can choose to adopt that new rule, and if a critical mass of people do so, then it is now a rule of the network.

People often think that because the protocol and the network itself has rules, that there is some kind of framework of “meta rules” surrounding that. That these meta rules must be followed in order to change the rules of the system itself, or are some kind of binding requirement to fulfill some purpose or nature of the system that cannot be changed or evolve over time. This completely fails to internalize the reality of what an anarchic system actually is. There are no rules except what people choose to voluntarily follow of their own accord.

Within the confines of those rules, it is anarchy. Anything anyone can voluntarily do in interaction with another person in the confines of those rules, is allowed. Even those rules themselves are simply the result of a consensus arrived at through a process of pure anarchy, i.e. people interacting voluntarily within the framework that they chose to. That is what it is, no matter how much you might want to twist and contort definitions in your head to fit some other framework.

There is no authority to appeal to here. There are no rules to demand people follow other than the consensus rules themselves, and even that cannot be demanded or enforced. All you can do is hope that people choose to continue following them out of their own self interest. At any time a persuasive individual or group can convince others to change even those. If that occurs, there is nothing whatsoever you can do about it except attempt to be more persuasive.

That is what anarchy is. Free association devoid of any type of authority, or coercion, or control over who other people associate with, or under what terms they choose to associate. Bitcoin is anarchy, and if that fact disturbs you or instinctually makes you want to argue against it, then the reality is you never understood Bitcoin in the first place.

Today, Ten31, a world leading bitcoin technology investor, has announced the Nasdaq Global Market stock exchange listing of its portfolio company, GRIID Infrastructure. This marks the first public listing for a bitcoin-focused investment fund's portfolio company, according to a press release sent to Bitcoin Magazine.

GRIID, a uniquely positioned, vertically integrated bitcoin mining and energy infrastructure company, has successfully navigated the long regulatory review process to achieve this public listing. Ten31, having served as GRIID's exclusive institutional capital partner, invested through its second institutional venture fund, Low Time Preference Fund II, underscoring its commitment to supporting innovative ventures in the bitcoin and freedom technology space.

“As a vertically integrated operator, purpose-built for bitcoin mining from day one, GRIID is uniquely positioned to become one of the leading bitcoin mining companies in the world,” said Trey Kelly, Founder and CEO of GRIID. “We believe that listing on Nasdaq will enhance our visibility, liquidity, and broaden our investor base as we continue to strengthen our market position and reinforce our commitment to delivering shareholder value. Ten31’s capital support and strategic guidance were invaluable in helping us reach this milestone. We feel strongly that there is no better partner or investor in the bitcoin space than Ten31, and we look forward to continuing our close partnership.”

In conjunction with GRIID's listing achievement, Ten31 welcomes Harry Sudock, GRIID's Chief Strategy Officer, as an Advisor while maintaining his role at GRIID. Sudock, a prominent figure in bitcoin mining and energy infrastructure, brings valuable expertise to Ten31's advisory team.

“After many years building a bitcoin company, I know firsthand the crucial value of capital partners that both share our understanding of bitcoin and offer proven institutional investment expertise. They embody bitcoin’s proof of work ethos in everything they do,” Sudock stated. “I expect GRIID to be the first of many success stories to emerge from the Ten31 portfolio, and I’m excited to help support Ten31 as it invests in the best companies in the rapidly evolving bitcoin ecosystem while serving as a resource to both portfolio companies and their founders.”

This development aligns with the launch of Ten31's third institutional fund, Low Time Preference Fund III, securing anchor commitments and fortifying its position as a leading bitcoin tech investor. Additionally, Ten31's Tactical Fund aims to provide access to individual accredited investors, offering further opportunities for participation in the rapidly evolving bitcoin ecosystem.

Ten31's commitment to supporting Bitcoin extends beyond investment in companies, as it continues to allocate funding to open-source development within the bitcoin ecosystem. The fund has granted support to independent bitcoin developer calle for his work on bitcoin-powered Chaumian ecash. Ten31 is the most active investor in open source businesses in the bitcoin ecosystem, and was a founding contributor to public charity OpenSats in 2021, supporting a variety of open source efforts on a no-strings-attached basis.

Today, Google has revised its advertising guidelines, now permitting cryptocurrency trusts, such as Bitcoin Exchange-Traded Funds (ETFs), to promote their products. Spot Bitcoin ETF issuers such as BlackRock and Franklin Templeton have wasted no time in marketing their funds, with advertisements already starting to emerge.

This revision comes at an interesting time as the discussion around Bitcoin ETFs continues to gains momentum, after the US Securities and Exchange Commission (SEC) approved the first batch of spot Bitcoin ETFs in the country. Google's decision to allow advertising for Bitcoin ETFs provides these financial instruments with a much broader reach and exposure to a wider audience.

The updated guidelines mean that companies managing Bitcoin ETFs can now leverage Google's advertising platform to raise awareness and attract investors. This change could contribute to increased visibility and understanding of Bitcoin ETFs among both institutional and retail investors.

Google's decision aligns with the growing acceptance of Bitcoin and related investment products in mainstream finance. The move is likely to help foster a more innovative environment for Bitcoin, as it integrates more into traditional financial markets. As the industry eagerly awaits to see how well these revised guidelines are for the Bitcoin ETFs, the impact on the advertising landscape for them could be substantial.

For the first time since launch, BlackRock's spot Bitcoin ETF is outpacing the Grayscale Bitcoin Trust (GBTC) in terms of trading volume so far today, according to Bloomberg ETF analyst James Seyffart.

BlackRock's spot Bitcoin ETF volume surpassing GBTC for the first time hints at a slow down in outflows for Grayscale's ETF, which has had over $5 billion in outflows since launch. As highlighted below, the other spot Bitcoin ETFs have had total gross inflows of over $5.8 billion.

This trend could mark a significant shift in suggesting that the selling of GBTC is weakening, thus easing their current massive selling pressure of Bitcoin. Other spot Bitcoin ETFs have experienced large amounts of inflows such as BlackRock and Fidelity, who have a combined 98,264 BTC worth over $4.1 billion for their ETFs.

As GBTC outflows lessen and inflows of other spot Bitcoin ETFs rise, BTC will continue to get taken off the market in record pace. To put this all into context, BlackRock have accumulated over 52,026 BTC since launch earlier this month. MicroStrategy, known for their aggressive Bitcoin accumulation strategy, have accumulated 189,150 BTC over the last ~four years.

As market participants eagerly wait in anticipation for the final numbers at the end of the day to see if the inflows on BlackRock's spot Bitcoin ETF can continue to outpace the outflows of GBTC, Bitcoin pumps over $43,000.

Significant shifts are underway in the ecosystem of illicit actors using cryptocurrency. According to a 2023 report by TRM Labs, Bitcoin is no longer the asset of choice for criminals.

The report states, “The multi-chain era has had a sweeping impact on the distribution of illicit crypto volume as a whole, where Bitcoin’s share plummeted from 97% in 2016 to 19% in 2022. In 2016, two thirds of crypto hack volume was on Bitcoin; in 2022, it accounted for just under 3%, with Ethereum (68%) and Binance Smart Chain (19%) dominating the field. And while Bitcoin was the exclusive currency for terrorist financing in 2016, by 2022 it was all but replaced by assets on the TRON blockchain, with 92%.”

Ramifications Of the Shift

Clearly, this turns the adage of Bitcoin being synonymous with criminal activity, on its head.

Since inception, Bitcoin has functioned as a Schelling Point due to its network effect, market dominance and liquidity, making it a natural choice in cryptofinance.

(In Game Theory parlance, a Schelling Point is a natural solution in situations where multiple parties must make decisions without direct communication. These points are intuitively obvious, often relying on shared expectations or common knowledge.)

However, now it seems that there is an ongoing separation of equilibria with bad actors opting for a different point of convergence.

Policy Takeaways

This move offers some key learnings from a policy perspective.

It highlights the need for policymakers to closely study specific assets and blockchains that are currently being favored by illicit actors and take appropriate action. More importantly, it provides an opportune moment to replace the current, generic perspective on digital assets with a more nuanced one, while shaping policy narratives on criminal usage.

Case in point, in the ongoing discussion on use of cryptoassets in terror financing, it often gets missed that Hamas has in fact stopped accepting Bitcoin donations, to protect its sponsors from being unveiled.

But most importantly, this shift of illicit finance away from Bitcoin, is the first ever documented case of major crime displacement in the world of cryptoassets. It sheds light on the fluid nature of Financial Crime as it adapts to the path of least resistance.

Perspectives From Game Theory

Consequently, a game-theoretic lens (with the players being - product devs, regulators, good and bad actors) enables a holistic and nuanced view of the space. We can see that in such a setting, interplay of independent actions and perspectives, generates myriad scenarios as the system is too intertwined for any set of players to control outcomes only by themselves.

A game-theoretic view of illicit finance expounds the need to step into the criminal mind to predict next steps and prepare accordingly. Policy making to combat illegal fund flows, is typically retroactive with bad actors making the first few moves, which are then studied as emerging risks to accordingly craft regulations. However, with the space of digital assets evolving at an exponential pace, we do not have the luxury of following this whack-a-mole approach (which happens to be the norm in designing Traditional Finance regulations).

The ongoing wave of crime displacement away from Bitcoin, highlights the necessity to arm policymakers with predictive systems that forecast future patterns of illicit fund flows. Such an approach will vastly minimize response time to new threats.

Counter-crime Initiatives

Lessons from Bitcoin’s changing usage, can also help counter-crime professionals grasp distinct features of organized crime syndicates. Case in point, crime rings still reliant on Bitcoin would signify a lack of agility in leadership. Additionally, position on an ‘agility spectrum’ can help infer further actionable insights about any syndicate, such its level of resourcefulness and technical expertise. This can also aid law enforcement in sizing the unique effort required in combating each crime ring. Case in point, crime syndicates which pioneered the shift away from Bitcoin, and are (consequently) ahead of the curve, would be operating at a relatively higher level of ingenuity, while continuously adapting to slip through the cracks.

Concluding Thoughts

The switch of financial crime away from Bitcoin, sheds light on the need of a more nuanced approach to curating apt and dynamic regulatory and policy frameworks for digital assets and blockchains. It also highlights the dangers of applying broad strokes to the entire spectrum of cryptofinance, when it comes to policy debates on criminal usage.

This is a guest post by Debanjan Chatterjee. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The following is a heuristic analysis of GBTC outflows and is not intended to be strictly mathematical, but instead to serve as a tool to help people understand the current state of GBTC selling from a high level, and to estimate the scale of future outflows that may occur.

Number Go Down

January 25, 2024 – Since Wall Street came to Bitcoin under the auspices of Spot ETF approval, the market has been met with relentless selling from the largest pool of bitcoin in the world: the Grayscale Bitcoin Trust (GBTC) which held more than 630,000 bitcoin at its peak. After conversion from a closed-end fund to a Spot ETF, GBTC’s treasury (3% of all 21 million bitcoin) has bled more than $4 billion during the first 9 days of ETF trading, while other ETF participants have seen inflows of approximately $5.2 billion over that same period. The result – $824 million in net inflows – is somewhat surprising given the sharply negative price action since the SEC lent its stamp of approval.

In trying to forecast the near-term price impact of Spot Bitcoin ETFs, we must first understand for how long and to what magnitude GBTC outflows will continue. Below is a review of the causes of GBTC outflows, who the sellers are, their estimated relative stockpiles, and how long we can expect the outflows to take. Ultimately these projected outflows, despite being undoubtedly large, are counterintuitively extremely bullish for bitcoin in the medium-term despite the downside volatility that we have all experienced (and perhaps most did not expect) post ETF-approval.

The GBTC Hangover: Paying For It

First, some housekeeping on GBTC. It is now plainly clear just how important of a catalyst the GBTC arbitrage trade was in fomenting the 2020-2021 Bitcoin bull run. The GBTC premium was the rocket fuel driving the market higher, allowing market participants (3AC, Babel, Celsius, Blockfi, Voyager etc.) to acquire shares at net asset value, all the while marking their book value up to include the premium. Essentially, the premium drove demand for creation of GBTC shares, which in turn drove bidding for spot bitcoin. It was basically risk free…

While the premium took the market higher during the 2020+ bull run and billions of dollars poured in to capture the GBTC premium, the story quickly turned sour. As the GBTC golden goose ran dry and the Trust began trading below NAV in February 2021, a daisy chain of liquidations ensued. The GBTC discount essentially took the balance sheet of the entire industry down with it.

Sparked by the implosion of Terra Luna in May 2022, cascading liquidations of GBTC shares by parties like 3AC and Babel (the so-called “crypto contagion”) ensued, pushing the GBTC discount down even further. Since then, GBTC has been an albatross around the neck of bitcoin, and continues to be, as the bankruptcy estates of those hung out to dry on the GBTC “risk free” trade are still liquidating their GBTC shares to this day. Of the aforementioned victims of the “risk free” trade and its collateral damage, the FTX estate (the largest of those parties) finally liquidated 20,000 BTC across the first 8 days of Spot Bitcoin ETF trading in order to pay back its creditors.

It is also important to note the role of the steep GBTC discount relative to NAV and its impact on spot bitcoin demand. The discount incentivized investors to go long GBTC and short BTC, collecting a BTC-denominated return as GBTC crept back up toward NAV. This dynamic further siphoned spot bitcoin demand away – a toxic combination that has further plagued the market until the GBTC discount recently returned to near-neutral post ETF approval.

With all that said, there are considerable quantities of bankruptcy estates that still hold GBTC and will continue to liquidate from the stockpile of 600,000 BTC that Grayscale owned (512,000 BTC as of January 26, 2024). The following is an attempt to highlight different segments of GBTC shareholders, and to then interpret what additional outflows we may see in accordance with the financial strategy for each segment.

Optimal Strategy For Different Segments Of GBTC Owners

Simply put, the question is: of the ~600,000 Bitcoin that were in the trust, how many of them are likely to exit GBTC in total? Subsequently, of those outflows, how many are going to rotate back into a Bitcoin product, or Bitcoin itself, thus largely negating the selling pressure? This is where it gets tricky, and knowing who owns GBTC shares, and what their incentives are, is important.

The two key aspects driving GBTC outflows are as follows: fee structure (1.5% annual fee) and idiosyncratic selling depending on each shareholder's unique financial circumstance (cost basis, tax incentives, bankruptcy etc.).

As of January 22, 2024 the FTX estate has liquidated its entire GBTC holdings of 22m shares (~20,000 BTC). Other bankrupt parties, including GBTC sister company Genesis Global (36m shares / ~32,000 BTC) and an additional (not publicly identified) entity holds approximately 31m shares (~28,000 BTC).

To reiterate: bankruptcy estates held approximately 15.5% of GBTC shares (90m shares / ~80,000 BTC), and likely most or all of these shares will be sold as soon as legally possible in order to repay the creditors of these estates. The FTX estate has already sold 22 million shares (~20,000 BTC), while it is not clear if Genesis and the other party have sold their stake. Taking all of this together, it is likely that a significant portion of bankruptcy sales have already been digested by the market aided in no small part by FTX ripping off the bandaid on January 22, 2024.

One wrinkle to add to the bankruptcy sales: these will likely not be smooth or drawn out, but more lump-sum as in the case of FTX. Conversely, other types of shareholders will likely exit their positions in a more drawn-out manner rather than liquidating their holdings in one fell swoop. Once legal hangups are taken care of, it is very likely that 100% of bankruptcy estate shares will be sold.

Next up, retail brokerage account shareholders. GBTC, as one of the first passive products available for retail investors when it launched in 2013, has a massive retail contingency. In my estimation, retail investors hold approximately 50% of GBTC shares (286m shares / ~255,000 bitcoin). This is the trickiest tranche of shares to project in terms of their optimal path forward because their decision to sell or not will depend upon the price of bitcoin, which then dictates the tax status for each share purchase.

For example, if the price of bitcoin rises, a greater proportion of retail shares will be in-profit, meaning if they rotate out of GBTC, they will incur a taxable event in the form of capital gains, thus they will likely stay put. However, the inverse is true as well. If the price of bitcoin continues to fall, more GBTC investors will not incur a taxable event, and thus will be incentivized to exit. This potential feedback loop marginally increases the pool of sellers that can exit without a tax penalty. Given GBTC’s unique availability to those early to bitcoin (therefore likely in profit), it is likely that most retail investors will stay put. To put a number on it, it is feasible that 25% retail brokerage accounts will sell, but this is subject to change depending upon bitcoin price action (as noted above).

Next up we have retail investors with a tax exempt status who allocated via IRAs (retirement accounts). These shareholders are extremely sensitive to the fee structure and can sell without a taxable event given their IRA status. With GBTC’ egregious 1.5% annual fee (six times that of GBTC’s competitors), it is all but certain a significant portion of this segment will exit GBTC in favor of other spot ETFs. It is likely that ~75% of these shareholders will exit, while many will remain due to apathy or misunderstanding of GBTC’s fee structure in relation to other products (or they simply value the liquidity that GBTC offers in relation to other ETF products).

On the bright side for spot bitcoin demand from retirement accounts, these GBTC outflows will likely be met with inflows into other Spot ETF products, as they will likely just rotate rather than exiting bitcoin into cash.

And finally, we have the institutions, which account for approximately 180,000 bitcoin. These players include FirTree and Saba Capital, as well as hedge funds that wanted to arbitrage the GBTC discount and spot bitcoin price discrepancy. This was done by going long GBTC and short bitcoin in order to have net neutral bitcoin positioning and capture GBTC’s return to NAV.

As a caveat, this tranche of shareholders is opaque and hard to forecast, and also acts as a bellwether for bitcoin demand from TradFi. For those with GBTC exposure purely for the aforementioned arbitrage trade, we can assume they will not return to purchase bitcoin through any other mechanism. We estimate investors of this type to make up 25% of all GBTC shares (143m shares / ~130,000 BTC). This is by no means certain, but it would reason that greater than 50% of TradFi will exit to cash without returning to a bitcoin product or physical bitcoin.

For Bitcoin-native funds and Bitcoin whales (~5% of total shares), it is likely that their sold GBTC shares will be recycled into bitcoin, resulting in a net-flat impact on bitcoin price. For crypto-native investors (~5% of total shares), they will likely exit GBTC into cash and other crypto assets (not bitcoin). Combined, these two cohorts (57m shares / ~50,000 BTC) will have a net neutral to slightly negative impact on bitcoin price given their relative rotations to cash and bitcoin.

Total GBTC Outflows & Net Bitcoin Impact

To be clear, there is a large amount of uncertainty in these projections, but the following is a ballpark estimate of the overall redemption landscape given the dynamics mentioned between bankruptcy estates, retail brokerage accounts, retirement accounts, and institutional investors.

Projected Outflows Breakdown:

250,000 to 350,000 BTC total projected GBTC outflows

100,000 to 150,000 BTC expected to leave the trust and be converted into cash

150,000 to 200,000 BTC in GBTC outflows rotating into other trusts or products

250,000 to 350,000 bitcoin will remain in GBTC

100,000 to 150,000 net-BTC selling pressure

TOTAL Expected GBTC-Related Outflows Resulting In Net-BTC Selling Pressure: 100,000 to 150,000 BTC

As of January 26, 2024 approximately 115,000 bitcoin have left GBTC. Given Alameda’s recorded sale (20,000 bitcoin), we estimate that of the other ~95,000 bitcoin, half have rotated into cash, and half have rotated into bitcoin or other bitcoin products. This implies net-neutral market impact from GBTC outflows.

Estimated Outflows Yet To Occur:

Bankruptcy Estates: 55,000

Retail Brokerage Accounts: 65,000 - 75,000 BTC

Retirement Accounts: 10,000 - 12,250 BTC

Institutional Investors: 35,000 - 40,000 BTC

TOTAL Estimated Outflows To Come: ~135,000 - 230,000 BTC

Note: as said previously, these estimates are the result of a heuristic analysis and should not be interpreted as financial advice and simply aim to inform the reader of what the overall outflow landscape may look like. Additionally, these estimates are pursuant to market conditions.

Gradually, Then Suddenly: A Farewell To Bears

In summary, we estimate that the market has already stomached approximately 30-45% of all projected GBTC outflows (115,000 BTC of 250,000-300,000 BTC projected total outflows) and that the remaining 55-70% of expected outflows will follow in short order over the next 20-30 trading days. All in, 150,000 - 200,000 BTC in net selling pressure may result from GBTC sales given that the significant proportion of GBTC outflows will either rotate into other Spot ETF products, or into cold storage bitcoin.

We are through the brunt of the pain from Barry Silbert’s GBTC gauntlet and that is reason to celebrate. The market will be much better off on the other side: GBTC will have finally relinquished its stranglehold over bitcoin markets, and without the specter of the discount or future firesales hanging over the market, bitcoin will be much less encumbered when it does arise. While it will take time to digest the rest of the GBTC outflows, and there will likely be a long tail of people exiting their position (mentioned previously), bitcoin will have plenty of room to run when the Spot ETFs settle into a groove.

Oh, and did I mention the halving is coming? But that’s a story for another time.

Bitcoin Magazine is wholly owned by BTC Inc., which operatesUTXO Management, a regulated capital allocator focused on the digital assets industry. UTXO invests in a variety of Bitcoin businesses, and maintains significant holdings in digital assets.

In the ever-evolving landscape of financial innovation, the recent approval of Bitcoin ETFs stands as a watershed moment, not just for digital asset enthusiasts, but for the broader financial markets and the political arena. As we edge closer to the 2024 elections, it's becoming increasingly clear that bitcoin is set to play a pivotal role in shaping the political discourse around digital assets, their regulation, and their integration into the mainstream financial ecosystem.

The Surge of Mainstream Adoption

Bitcoin, once a niche interest of tech enthusiasts and libertarians, has catapulted into the limelight, thanks to the sustained growth in adoption and the recent introduction of Bitcoin ETFs. This groundbreaking development is not merely a triumph for Bitcoin advocates; it signifies a leap towards widespread acceptance and normalization of digital assets. By providing a regulated and familiar investment vehicle for Bitcoin, these ETFs bridge the gap between traditional finance and the burgeoning world of digital assets, making Bitcoin accessible to a broader range of investors, including institutions.

The involvement of institutional investors in Bitcoin ETFs brings a level of legitimacy and stability that was previously elusive in the cryptocurrency market. Institutions like pension funds, endowments, and large asset managers are known for their rigorous due diligence processes and conservative investment strategies. Their entry reflects a broader acceptance of Bitcoin and cryptocurrency as a legitimate asset class, one that merits inclusion among traditionally conservative financial entities.

The mainstreaming of Bitcoin is poised to have profound implications for the 2024 elections. For the first time, Bitcoin and digital assets are likely to emerge as a significant policy issue, one that candidates cannot afford to overlook. As more individuals and institutions invest in Bitcoin, public interest in the regulatory and policy framework governing digital assets is surging. This heightened interest will compel political candidates to develop and articulate clear positions on Bitcoin and cryptocurrency, framing it as a critical component of their economic and technological platforms. Regulatory clarity and robust policy frameworks for digital assets will become key talking points in election campaigns.

Digital Asset Policy And Regulation At The Forefront Of The 2024 Elections

The 2024 elections will likely see intense debates over the future direction of the U.S. and global economies, with digital currencies playing a key role. Policies surrounding Bitcoin and digital assets will be indicative of broader economic strategies, touching on issues of financial inclusion, the digitalization of the economy, and the U.S.'s competitive position in the global financial technology race.

The integration of Bitcoin into mainstream finance brings with it a host of regulatory challenges and questions. Issues like consumer protection, market stability, anti-money laundering (AML) policies, and cross-border transactions are just the tip of the iceberg. Candidates will need to navigate these complex issues, balancing the need for innovation-friendly policies with the imperative of protecting investors and maintaining financial stability. Furthermore, candidates in the 2024 elections will have to consider the U.S.'s position in the global economy, addressing issues like international cooperation on regulatory standards and the competition to attract and retain digital asset businesses. The most near term issue is that of AML and terrorist financing that was surfaced by the error-filled WSJ article and has been parroted by Senator Warren an untold number of times. Accurate data, and pushing back against the fear mongering of people like Elizabeth Warren is more easily done from the bully pulpit of the Presidency.

Shifting Voter Sentiments And Demographics

As Bitcoin becomes a mainstream financial instrument, its influence extends beyond investment portfolios to the very heart of voter sentiment. The burgeoning class of digital asset investors, ranging from tech-savvy millennials to institutional stakeholders, represents a significant and influential demographic. Their concerns and interests in digital currency policy are likely to shape the political landscape in 2024, forcing candidates to engage with a broader range of economic issues, including the future of decentralized finance and the role of digital assets in the economy.

The evolution of voter demographics and sentiments heralds a new era in political campaigning, where understanding and addressing the nuances of digital finance becomes imperative. Candidates will find themselves navigating a complex landscape where traditional economic policies intersect with emerging digital financial technologies. To resonate with this growing voter base, candidates will need to demonstrate not only an understanding of digital assets and their implications but also present forward-thinking strategies that integrate these technologies into their economic visions. Americans under the age of 30 are seven times more likely to own digital assets than an American over 65. Based on polling in Texas, we see that this trend cuts evenly across party lines.

This shift in voter base also raises the bar for political discourse, demanding a more nuanced understanding of technology among political figures. No longer can digital assets be sidelined as a niche interest; they now represent a crucial component of economic discussions that can sway voter opinions. Candidates who adeptly navigate these discussions, offering innovative yet pragmatic solutions, are likely to gain traction among this pivotal demographic. The 2024 elections stand at the crossroads of traditional finance and the burgeoning digital asset industry, signaling a transition towards a political landscape increasingly shaped by Bitcoin, digital asset, and financial innovation.

The Role Of Educational Outreach And Advocacy

As the implications of Bitcoin ETFs permeate the mainstream, there's an increasing need for educational outreach and advocacy. Both the public and policymakers must be informed about the nuances of Bitcoin, digital currencies and blockchain technology. This education will play a crucial role in shaping informed public opinion and, consequently, the electoral choices of voters. Organizations and advocates within the digital asset space will have an important role to play in this education and advocacy effort, helping to demystify digital assets for the wider public and policymakers alike. In this dynamic environment, the leadership shown by key regional councils in advancing blockchain understanding and advocating for sound policies sets a benchmark in driving the conversation forward, showcasing the potential of focused expertise and strategic foresight in shaping the future of Bitcoin and digital assets.

Conclusion: A New Era Of Politics

The approval of Bitcoin ETFs is more than just a milestone for the digital asset market; it's a harbinger of a new era in political discourse. The mainstream adoption of Bitcoin and other digital currencies will force a reevaluation of economic policies, regulatory frameworks, and even the very nature of financial systems. Candidates in the 2024 elections will need to navigate this new landscape, addressing the complexities of digital assets while resonating with a voter base that is increasingly informed and influenced by the world of cryptocurrency. As we approach the 2024 elections, the intersection of Bitcoin, digital assets, blockchain, and politics is not just a passing trend but a fundamental shift in the fabric of economic and political life.

This is a guest post by Mark Shut. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Is it really surprising, given that cats have essentially dominated the internet for the last two decades, that cat memes have finally taken over the Bitcoin space as well in the last few weeks? Cats are the most viral meme on the internet, so it's not shocking in the least bit that the Taproot Wizards have leaned into it, reinforced by the trolling Luke over his “dietary choices.”

The question has to be asked though, are meme campaigns really how we want to go about deciding and discussing consensus changes to a protocol as valuable as Bitcoin? I’ve seen numerous music videos, campaigns to go out in the world and “educate” people on OP_CAT, and the whole “Quest” system that Taproot Wizards has launched taking place…but the reality is the vast majority of this content that I have seen has been incredibly superficial.

Rijndael, “Artificer” at Taproot Wizards and one of the few people, if not the only person, actually tinkering and playing with OP_CAT to build out use case examples, has made a demo of a OP_CAT based covenant script.

This script enforces a specific amount of Bitcoin be sent to a specific address, and by consensus there is no other way to spend these coins except with a transaction that meets those exact conditions. Look at the size of this script:

This is what it takes to emulate CHECKTEMPLATEVERIFY. The equivalent script using CTV would simply be:

CTV <32 byte hash>.

I ask, what is the value of something like OP_CAT in emulating the case of basic template covenants (things requiring a spending transaction to fulfill certain conditions defined ahead of time to be valid) like this? We know exactly how to handle schemes enforcing a template on transactions spending an output locked to a template covenant, and have multiple proposals for them. CTV, TXHASH, OP_TX, and even APO can emulate these schemes by stuffing a signature in the locking output of a transaction at the cost of an extra 64 bytes.

What actual use is OP_CAT in “experimenting” to meet the needs of a class of use cases that are mature enough in design that there are at least 4 covenant proposals that can handle those use cases with a tiny fraction of the data cost? “Oh, we want to experiment with CAT because it’s flexible!” You want to use 30 OP calls to do something that can be done in one? That is a reason to actually enact a consensus change to Bitcoin? The logic of that is beyond absurd.

Downplaying Risks

In a vacuum OP_CAT is sold as “simply concatenating two strings”, and many of the memes attempt framing it as “how can that be dangerous?” This is a wildly disingenuous narrative surrounding the proposal, and it completely ignores how it interacts with other existing and future aspects of script.

In particular CSFS + CAT opens a massive amount of possibilities in terms of what can be done with Bitcoin script, not all of it necessarily positive. CSFS allows you to verify a signature on an arbitrary piece of data in the course of executing a script, and CAT allows you to “glue” different pieces of data together on the stack. These two things create a massive design space for what it is possible to do with Bitcoin.

One concrete example would be the potential to enforce amounts, or relationships between different amounts, of specific inputs and outputs in a transaction. CAT allows you to build up a transaction hash from individual pieces on the stack, and CSFS allows you to verify a signature against a public key in the locking script against arbitrary pieces of that transaction as it is built up. This could ultimately enable the creation of open-ended UTXOs anyone can spend, as long as the spending transaction meets certain criteria, such as a specific amount of coins be sent to a specific address. Combine this with the reality of OP_RETURN based assets, and this starts getting into the territory of Decentralized Exchanges (DEX).

Some of the worst incentive distortion problems that have come to fruition on other blockchains ultimately stem from the creation of DEXes on those chains. Having direct non-interactive exchange functionality on the blockchain is one of the worst forms of MEV, especially when the potential exists for miners to lock-in their profit across multiple trades in the span of a single block, rather than having to actually carry the risk of a position across multiple blocks before closing it out and realizing profit.

Part of the movement behind Taproot Wizards is “bringing the innovation back.” I.e. that lessons learned in shitcoin land are coming home to Bitcoin, now while I firmly reject the notion that anything useful has been developed on other coins in the last decade other than the basic concept of zero knowledge proofs, this mantra getting louder ignores a massive component of that dynamic even if you disagree with my view there: there are lessons to be learned regarding what NOT to do as well as what TO do.

DEXes are one of the things NOT to do. Nothing has caused as much chaos, volatility in fee dynamics (which we need to smooth out over time for sustainability of second layers), and just all around incentive chaos regarding the base consensus layers of these protocols and their degree of centralization. The idea that we should rush to bring these types of problems to Bitcoin, or exacerbate them by introducing a way to trustlessly embed the bitcoin asset into them in more dynamic and flexible ways, is frankly insane. This to me speaks of large swaths of people who haven’t learned anything from watching what happened on other blockchains in the last half decade or so.

Forever Shackled By The Cat

Looking at the dynamic above between CSFS + CAT, it is worth pointing out that Reardencode’s recent LNHANCE proposal (CTV + CSFS + Internal Key) offers a path to give us eltoo for Lightning in a way that is actually more blockspace efficient than using APO. If this argumentation, and build out of proof of concepts, winds up winning over Lightning developers who want LN symmetry in order to simplify Lightning channel management and implementation maintenance, we very well could wind up getting CSFS in the process. If OP_CAT were active prior to this, then there is no way to avoid the types of detrimental side effects of the two proposals being combined.

This would hold true for every soft fork proposal going forward if OP_CAT were ever activated. It would be impossible to escape whatever side effects or use cases were enabled by combining OP_CAT with whatever new proposals come in future. On its own OP_CAT is clunky, inefficient, and rather pointless. But in combination with other OPs it begins to get stupidly flexible and powerful. This would be a dynamic we would never be able to escape, and features that might wind up being critically necessary in the future for Bitcoin’s scalability could inescapably come with massive downsides and risks simply because of the existence of OP_CAT.

Is this a reality we want to enter simply because of a meme campaign? Because people want to tinker with wildly inefficient means of doing things instead of looking through much more efficient and purpose built proposals? I would say no.

Meme campaigns can be fun, I know this. They foster a sense of community and involvement, it's an inherent and inescapable part of the internet and the numerous cultures that exist on it. But this is not how we should be deciding the development process of Bitcoin. They can be fun, and they can even be viciously savage at stabbing directly to the heart of matters people dance around or equivocate on. But they are atrocious at capturing nuance and complexity in many regards.

Trying to steer the consensus of a network like Bitcoin purely based on the value of a meme, rather than reasoned consideration of proposals and their implications, is a disaster waiting to happen. The conservatism and caution of Bitcoin development is what has kept it at the forefront of this space as shitcoins have come and gone, imploding in the consequences of their fly by night carefree development attitude. As much as Bitcoin sorely needs to break out of its current rut of stagnation and lack of forward progress, devolving to uncritical memes and music videos is not how to do that. It risks destroying what made Bitcoin valuable in the first place, its solid and conservative foundation.

Today, BTC-only exchange Swan Bitcoin unveiled its new mining division, Swan Mining, which was previously operating in stealth mode, according to a press release sent to Bitcoin Magazine. The division is now positioned under Swan Institutional, with a focus on securing the Bitcoin network while contributing to the expansion of energy production and stabilization of electrical grids.

Having commenced operations in Summer 2023, Swan Mining is already a substantial contributor to the Bitcoin network, providing 4.5 exahash, according to the release. With plans to enhance its capacity to over 8 exahash, the unit has rapidly purchased and deployed mining equipment, expecting full deployment by March. Notably, Swan Mining stated it has already successfully mined over 750 bitcoin.

“We are proud to play a role in keeping Bitcoin mining decentralized,” said Rapha Zagury, Swan CIO and head of Swan Mining. “Our understanding is that this is the fastest-ever initial deployment of hashrate at this scale in Bitcoin history. With hard work and a little luck, we hope Swan Mining will help to secure the network for many decades.”

Zagury further stated that to avoid causing disruption in ASIC pricing, Swan Mining first launched in stealth mode, which also allowed the company to develop its strategy to partner with operators in the space.

Swan's mining business follows a funding model with no debt, with entities legally segregated from the rest of Swan's operations. The launch of Swan Mining is also playing a important role in the growth of Swan Institutional, the company stated, fostering strategic partnerships with major industry players. Swan's institutional unit supports capital raises and balance sheet restructuring, aiming to unlock notable operational and financial potential for its partners.

“Swan Mining is a great example of our company thesis playing out,” said Swan founder and CEO Cory Klippsten. “With our exclusive focus on Bitcoin adoption and helping the industry grow, we continue to attract the talent, opportunities, and capital required to launch new business lines and grow them rapidly.”

Riding on a year of substantial expansion, Swan Bitcoin has doubled its team size and grown revenue to over $125 million annualized, according to the release. With plans to raise Series C financing in the coming months, Swan Bitcoin intends to allocate capital equally between financial services, mining, and acquisitions. Swan Bitcoin's CEO, Cory Klippsten, also disclosed the company's active pursuit of a public listing within the next 12 months.

The transition from Fiat Standards to the Bitcoin Standard, though highly desirable, is not inevitable or necessarily imminent. The timing and occurrence of these changes hinge on the adoption choices made by individuals, organizations, and public entities. These decisions are influenced not only by rational considerations but also by emotional and irrational factors (greed and fear above all). The collective will, formed by the intentions of a critical mass with sufficient capital and agency, plays a crucial role in displacing central banks and the entrenched power structures in favor of a new system centered around Bitcoin. Despite Bitcoin's evident technical, economic, and ethical superiority over other form of money, this struggle will undoubtedly be a formidable one, with the outcome far from assured.