According to its CEO, the exchange grew too quickly to accommodate the fast-growing crypto ecosystem.

Cryptocurrency exchange Kraken announced on Nov. 30 that it has made one of its “hardest decisions” and is cutting down its global workforce by approximately 1,100 people, comprising approximately 30% of its total workforce, amid current market conditions.

According to CEO and co-founder Jesse Powell, Kraken had to triple its workforce due to the fast-growing crypto ecosystem, and the current pullback takes the size of the company’s team back to where it was 12 months ago. Powell shared in a tweet, "Macro was already tough and we held out but recent industry woes diminished near-term optimism about a crypto rebound."

Rough day at @krakenfx. Headcount rolled back 12 mos. Macro was already tough and we held out but recent industry woes diminished near-term optimism about a crypto rebound. Better positioned now. Glad we were able to take good care of our former colleagues. Been a privilege. ♂️ https://t.co/xfwShapS2N

Lower trading volumes and fewer client sign-ups amid turbulent market conditions have contributed to Kraken’s decision to cut down its expenses by slowing down hiring efforts and avoiding large marketing commitments.

According to the exchange, these changes are necessary “to sustain the business for the long-term while continuing to build world-class products and services in selective areas that add the most value for our clients.”

The company stated that employees being let go were given a decent severance package, which includes separation pay covering 16 weeks of base pay, performance bonuses, four months of healthcare coverage including counseling, immigration support and career support, among other benefits.

Earlier this year in June, Kraken announced that it would continue to hire over 500 roles in various departments amid a market downturn. The company's hiring efforts were at the time in stark contrast to major layoff announcements from major blockchain firms such as Coinbase and BlockFi.

In support of the decision to continue to expand its staff earlier in the year, Kraken had said:

“We have not adjusted our hiring plan, and we do not intend to make any layoffs. We have over 500 roles to fill during the remainder of the year and believe bear markets are fantastic at weeding out the applicants chasing hype from the true believers in our mission."

Current layoffs, however, show a contrasting picture from the CEO's statements made in June, when he took the opportunity to throw shots at supposed “woke activists" while discussing the company's decision to hire hundreds of new employees.

FTX US won a $1.4-billion bid to purchase Voyager’s assets in September, but with the firm filing for bankruptcy, the funds were once again up for grabs.

Trading platform INX has submitted a bid for an undisclosed amount to purchase the assets of crypto brokerage firm Voyager Digital.

In a Nov. 30 announcement, INX said it had sent a non-binding letter of intent for Voyager’s assets following the platform filing for bankruptcy in July. According to INX CEO Shy Datika, the bid was aimed at providing “credibility, technology, and unique regulatory positioning” for Voyager users seeking stability in a volatile market.

Voyager’s original bankruptcy filing from the Southern District Court of New York suggested the firm could owe between $1 billion to $10 billion to more than 100,000 creditors amid a bear market and exposure to Three Arrows Capital. In September, FTX US won a $1.4-billion bid to purchase Voyager’s assets, but with FTX Group itself filing for bankruptcy in November, the funds were once again up for grabs.

Binance has reportedly been considering a bid for Voyager’s assets, while crypto exchange CrossTower was one of the firms that made an offer prior to FTX’s downfall. Cointelegraph reported on Nov. 13 that CrossTower had been working on a revised bid following FTX Group’s bankruptcy filing. INX was not part of the bidding process in September.

Cointelegraph reached out to INX for comment, but did not receive a response at the time of publication.

British-American businessman John McAfee talks about his crypto story and how he discovered BTC.

From the Cointelegraph archives, John McAfee tells his crypto story and takes a look back at his very fascinating life.

Early in his life, the computer programmer landed a job at the United States National Aeronautics and Space Administration, also known as NASA, and worked on the world’s first weather satellite. There, he learned about computer security and people’s concerns over unauthorized actors gaining access to private data.

McAfee also shared that he made all his money not from the popular “McAfee” antivirus software but from other projects. He explained:

“People know me from McAfee, but no, that was not my greatest success. That was some trivial thing. It was my future things, which I did not attach my name to, that taught me and made me all of my money.”

In 2011, McAfee’s friends pressured him into reading the Bitcoin (BTC) white paper published by its pseudonymous creator Satoshi Nakamoto. The computer programmer was impressed with the power of Bitcoin’s mathematics and saw the digital asset’s world-changing potential.

According to McAfee, his entry to crypto started with being the chairman and CEO of MGT, which was the world’s sixth largest BTC mining firm, valued at $800 million. However, McAfee noted that it eventually folded when BTC sank after going sky-high.

The company was delisted by the New York Stock Exchange, which McAfee claimed was a warning shot — an attempt to silence him and a threat that he would be destroyed if he didn’t be quiet. McAfee continued the story:

“First of all, they tried to collect me in America when they convened a grand jury. I found out about it beforehand, so we left the following day to Florida. We picked up our yacht with Janice, myself, four large dogs and seven of my staff and sailed away, went to the Bahamas.”

McAfee said that they eventually went to Cuba and then to the Dominican Republic, where they were arrested before getting off the boat.

Developers say the tool can help users save upwards of 15% on gas fees when shopping for NFTs.

According to a new post on November 30, decentralized exchange (DEX) Uniswap announced that users can now trade nonfungible tokens, or NFTs, on its native protocol. As told by Uniswap, the function will initially feature NFT collections for sale on platforms including OpenSea, X2Y2, LooksRare, Sudoswap, Larva Labs, X2Y2, Foundation, NFT20, and NFTX.

"To bring users the first-rate experience they've come to expect with Uniswap, we built the aggregator to deliver better prices, faster indexing, more unassailable smart contracts, and efficient execution."

Uniswap developers claim that users can save up to 15% on gas costs compared to other NFT aggregators when using Uniswap NFT. unifies ERC20 and NFT swapping into a single swap router. Integrated with Permit2, users can swap multiple tokens and NFTs in one swap while saving on gas fees.

The NFT aggregator is powered by the Universal Router smart contract and optimized by UX smart contract Permit2, both Uniswap inventions. According to the DEX, it "unifies ERC-20 and NFT swapping into a single swap router. Integrated with Permit2, users can swap multiple tokens and NFTs in one swap while saving on gas fees."

"We originally conceived Permit2 and Universal Router to improve our own products, optimizing gas costs, simplifying user transaction flows, and strengthening security. As we ideated, we realized that other applications could greatly benefit from integrating these contracts."

As part of launch efforts, Uniswap says it is airdropping approximately 5 million USDC to certain historical users of NFT aggregator Genie, based on a wallet snapshot on April 15, 2022, and offering gas rebates to the first 22,000 NFT users. However, the gas rebate will only run for two weeks and is capped at 0.01 Ether (ETH).

Taran’s death is the third to shake the crypto world in recent weeks, following Amber Group’s Tiantian Kullander and MakerDao’s Nikolai Mushegian.

Russian billionaire Vyacheslav Taran, president of Libertex Group and founder of Forex Club, died Nov. 25 in a helicopter crash in France while en route from Lausanne to Monaco, Switzerland. He was 53. The helicopter pilot, the only other person aboard the craft, also died.

“It is with great sadness that Libertex Group confirms the death of its co-founder and Chairman of Board of Directors, Vyacheslav Taran, after a helicopter crash that took place en route to Monaco on Friday, 25 November 2022.”

Taran, who was trained as a radio engineer, founded the foreign exchange trading platform Forex Club in Russia in 1997. Forex Club became one of the three leading exchanges in the country before the Russian Central Bank closed it and a number of other exchanges in December 2018 for irregularities in their registrations. Forex Club Group continues to operate in more than 100 other countries.

The Libertex trading platform was established in 2012 as part of the Forex Club Group and registered in Cyprus. It offers a wide range of financial products, including cryptocurrency trading and “in-app crypto mining software” and is a sponsor of Bayern Munich football club. According to Russian media, Taran was associated with the YouHodler wallet and Wirex app and card, as well as several other investment and real estate companies.

Taran was also the founder of the Change One Life charitable foundation, which provides assistance to Russian orphans and adoptive families.

Russian billionaire, 53, is killed in helicopter crash near Monaco in latest crypto mystery death - 'after another passenger cancelled at the last minute'

Vyacheslav Taran, 53, died after the helicopter he was travelling in crashed near the resort town of pic.twitter.com/LwGX089ttM

Taran is the third crypto executive to die unexpectedly in recent weeks. Amber Group cofounder Tiantian Kullander (TT) died Nov. 23 in his sleep at the age of 30, and MakerDAO cofounder Nikolai Mushegian drowned in Puerto Rico Oct. 28 at the age of 29. Taran is also the latest in a longer string of Russian businessmen to die under various circumstances.

Taran’s death has led to some speculation in the press. The helicopter accident that claimed Taran’s life in under investigation; It took place in good weather conditions with an experienced pilot. According to France Bleu, a second passenger was booked for the flight but cancelled at the last minute.

The Ukrainian new agency Unian alleged, “According to press accounts, Taran was a staff specialist of Russian foreign intelligence and was responsible for laundering Russian Federation funds through a system of cryptocurrency operations.” Unian did not provide links to those media. It stated his net worth at $20.2 billion.

Taran is survived by his wife Olga and three children, including an adopted son.

On-chain activity suggests that the hacker has sent at least 225 BTC (4.5 million) to OKX so far.

Hackers who drained FTX and FTX USA of over $450 million worth of assets just moments after the doomed crypto exchange filed for bankruptcy on Nov. 11, continue to move assets around in an attempt to launder the money.

A crypto analyst who goes by ZachXBT on Twitter alleged that the FTX hackers have transferred a portion of the stolen funds to the OKX exchange, after using the Bitcoin mixer ChipMixer. The analyst reported that at least 225 BTC — worth $4.1 million USD — has been sent to OKX so far.

1/ Myself and @bax1337 spent this past weekend looking into the FTX attacker’s deposits to ChipMixer.

It appears they’ve likely been transferring a portion of the stolen FTX funds to OKX after withdrawing from CM

According to ZachXBT, the FTX hacker first began depositing BTC into ChipMixer on Nov. 20, after using Ren Bridge, a protocol that acts as a bridge for cryptocurrencies. In his analysis, ZachXBT shared that he had observed a pattern with addresses receiving funds from ChipMixer. According to him, each of the addresses follows a similar pattern; “withdrawal from CM”, “50% peels off” and then “50% deposited to OKX”.

Following the discovery of the deposits made to the OKX exchange, the Director of OKX shared on Twitter that; “OKX is aware of the situation, and the team is investigating the wallet flow.”

#OKX is aware of the situation, and the team is investigating the wallet flow.

On Nov, 12, Cointelegraph reported that the hack was flagged right after FTX announced bankruptcy. At the time, out of the $663 million drained, around $477 million were suspected to be stolen, while the remainder is believed to be moved into secure storage by FTX themselves.

On Nov. 20, the hacker began transferring their Ether (ETH) holding to a new wallet address. The FTX wallet drainer was the 27th largest ETH holder after the hack, but dropped by 10 positions after dumping 50,000 ETH.

The fact that hackers managed to drain assets from FTX global and FTX.US at the same time, despite these two entities being completely independent, became a hot topic of discussion within the crypto community, and raised speculations about it possibly being an inside job.

Sergey Vasylchuk, the CEO of Everstake, said individuals behind Russian propaganda used the fall of FTX "to spin yet another tale about money laundering."

Everstake, a blockchain firm that partnered with the Ukrainian government to launch a donation website amid the country’s war with Russia, has pushed back against online rumors and conspiracy theories that the platform was used for politically motivated money laundering.

Ukrainian government officials partnered with Everstake, Kuna and the now infamous crypto exchange FTX to launch Aid for Ukraine in March following the Russian military’s invasion. According to the platform, crypto users and Ukraine supporters sent roughly $60 million in crypto and fiat aimed at supporting Ukraine’s armed forces and other humanitarian causes. However, with FTX’s liquidity issues and bankruptcy, Sam Bankman-Fried seemingly falling from grace, and possible legal action against the firm and its executives, social media users have taken many liberties with the truth speculating over the final destination of the crypto donations.

The conspiracy theories promulgated online falsely claim that due to its association with FTX and Bankman-Fried’s previous political donations, Aid for Ukraine’s funds ended up being funneled to the United States Democratic Party. An Everstake spokesperson branded such rumors as Russian propaganda, which was spread by North Carolina Representative Madison Cawthorn’s Twitter account, and “biased media, like Fox News and Russia Today.”

According to Everstake, the false claims do not “correspond with reality” given that the majority of the funds already went towards helmets, bulletproof vests, and night vision technology for Ukraine’s military, as the country’s Deputy Prime Minister Mykhailo Fedorov reported in August. The spokesperson added that the situation with FTX “does not affect the operation of Aid For Ukraine,” as the platform only used the exchange “a few times” to convert crypto donations to fiat in March and had no funds stored on FTX at the time of its collapse.

“Every time Russia is defeated on the battlefield, it starts looking for another way to cover up its military failures in the media by spreading fake news based on made-up assumptions,” said Everstake CEO Sergey Vasylchuk. “This time, they decided to use the collapse of FTX to spin yet another tale about money laundering. It is obvious that Western support of Ukraine hurts Russia as it leads to its losses on the battlefield. We know for a fact that every donation was spent for the benefit of Ukraine.”

A fundraising crypto foundation @_AidForUkraine used @FTX_Official to convert crypto donations into fiat in March. Ukraine's gov never invested any funds into FTX. The whole narrative that Ukraine allegedly invested in FTX, who donated money to Democrats is nonsense, frankly ♂️

One of the kernels of truth within the rumor surrounds Bankman-Fried admitting to being a “significant donor” for political candidates in the U.S. 2022 midterm elections, but with the majority of his contributions going towards Democrats. On Nov. 29, the Texas Tribune reported that Texas gubenatorial candidate Beto O’Rourke — a Democrat who lost his race against incumbent Greg Abbott — returned a $1 donation from SBF prior to election day.

"I wish I could have pulled that off," Bankman-Fried jokingly said in a Nov. 16 interview with Tiffany Fong addressing the rumors. "I was helping Ukraine launder funds for the Democratic Party? [...] I wished I was part of an international conspiracy that interesting."

Speaking to Cointelegraph, Vasylchuk said that Ukrainian government officials had been forced to respond to “serious people” inquiring about the online rumors. The Everstake CEO speculated that recent shakeup at Twitter amid Elon Musk taking over as CEO had further opened the doors for conspiracy theories to run amok on the platform, like the one related to FTX and Ukraine’s crypto donations.

“Society is blind to stop the spread of lying and propaganda,” said Vasylchuk. “We see how propaganda can influence like in Russia — [they fooled] millions of people. At the same time, I see them turn to [fooling] Americans, and social media can do the same. So, I’m really scared. I’m scared for the information and scared how it’s easy to manipulate or to force people to believe some type of this information.”

He added:

“This information was similar to information like ‘Ukraine developed battle mosquitoes which will bite Russians’ [...] I was thinking that American society is much more mature than it is in [Europe], and the people are actually able to feel the reality, the obvious bullshit, but unfortunately not.”

Vasylchuk reported that crypto donations through Aid for Ukraine had tapered off in recent months. Many crypto users are expected to send cash and tokens to various organizations as part of Giving Tuesday, or Bitcoin Tuesday, on Nov. 29.

The project shared that “a community-wide effort to fork Serum is going strong,” however.

The Solana-based decentralized exchange (DEX) has notified its community that the collapse of its backers — Alameda and FTX — has rendered its program “defunct”.

The team behind the project shared that “there is hope”, in spite of its ongoing challenges, because of the community option available to "fork" Serum.

According to the announcement, “a community-wide effort to fork Serum is going strong”. OpenBook, the community-led fork of the Serum V3 program, is already live on the Solana Mainnet with over $1M daily volume, supported by continuous efforts to expand it and grow its liquidity.

The existence of OpenBook however poses a threat to Serum, because “with Openbook's existence, Serum's volume and liquidity has dropped to near-zero” as users and protocols prefer Openbook because it’s a safer option following the security risks associated with the “old Serum code” which was compromised in the FTX hack.

When it comes to its SRM token, the DEX shared that the “future of SRM is uncertain”, as community members appear divided on the subject. Some believe it should still be used “for discounts”, while others believe it should not be used at all due to its exposure to FTX and Alameda.

On Nov 12, Cointelegraph reported that FTX was hacked with wallets tied to FTX and FTX US drained of $659 million in cumulative outflows, as reported by Nansen.

Following the FTX hack, Solana’s developers forked the widely used token liquidity hub, Serum, after it was compromised in the series of unauthorized transactions. On Nov 12, Solana co-founder Anatoly Yakovenko tweeted that developers depending on Serum were forking the code after the upgraded key was compromised, sharing that many “protocols depend on serum markets for liquidity and liquidations.”

After a week in El Salvador, it’s clear that state-run Bitcoin adoption is a slow but critical foundation for revitalizing the country.

This is an opinion editorial by Shinobi, a self-taught educator in the Bitcoin space and tech-oriented Bitcoin podcast host.

I recently spent a week in El Salvador to attend Adopting Bitcoin and decided it might be worthwhile to summarize my perception of things having actually had the chance to visit the country myself.

Since the announcement of the Bitcoin legal tender law in 2021, the topic of El Salvador has been a deeply divisive one in this space. On one hand, you have people blindly cheering on President Nayib Bukele and treating all criticism as FUD and misinformation generated simply to attack Bitcoin and the use of it. On the other hand, you have people blindly decrying him as a dictator and violator of human rights and treating anything positive he is accomplishing for his country as irrelevant in the face of his disregard for law.

Obviously, I am not a Salvadoran. I have never lived in the country and the short amount of time I have now spent there is by no means enough to truly acquire a deep insight into what life is like in El Salvador, or to really appreciate the nature of the problems people face there. Nevertheless, seeing things for that short time in person has given me a very different perspective than the one I had purely informed by reading things over the internet.

Adoption Has Been Slow, But The Seed Is Planted

I was very skeptical of the Bitcoin law when it was first proposed. My first article for Bitcoin Magazine was actually about my worries over ways the law could cause negative consequences and effectively implode on itself if adoption of Bitcoin took off too fast early on. I saw the promise of conversion to USD by the government of El Salvador as something that could fail catastrophically if Bitcoin became a major vehicle for remittance payments, effectively bankrupting the trust established for conversion on the dollar side. Thankfully, that did not happen.

Adoption seems to be a very slow-moving wave in the country, and according to many people I talked to when I was there, many businesses that used to accept bitcoin have actually stopped accepting it over the last year or so. Chivo is still dealing with problems, to the point that even today there are still issues with the ATMs during attempts to sell, and horrible UX flows make paying at the few businesses that accept BTC an annoying experience. It is by no means "Bitcoin country," as people constantly call it, in the sense of being able to use Bitcoin everywhere. But the opportunities to use it in El Salvador do far exceed those of any other physical locality I have ever traveled to myself. The plant hasn't quite sprouted yet, but the seed is clearly in the ground.

Bukele Is Going Beyond Bitcoin

Beyond the debates over Bitcoin use and adoption though, Bukele has done quite a lot in the last year. I feel like people in this space pontificating on the internet lose sight of this in arguing over the adoption of Bitcoin in El Salvador, but what is being done in the country goes beyond just Bitcoin. Bitcoin is a part of the plan, yes, but this is a nation of more than six million people for whom President Bukele is responsible. His concern isn't, and should not be, purely to benefit Bitcoin with his actions in office. He has the citizens of El Salvador and their wellbeing to concern himself with. That is his primary concern.

When I was in El Salvador for Adopting Bitcoin, I met someone who has been living in the country for the last 10 years who only recently got into Bitcoin because of the Bitcoin Law passed by Bukele a year ago. He had almost a decade of experience living in El Salvador as it was before Bukele, and the reality of it as he described was much more brutal than any statistics could paint: street merchants being murdered over not being able to afford 16 cents of protection money, widespread racketeering and robbery, corruption all across the government. Gang members would commit a murder, get arrested, and be out on the street within a few months due to how easy it was to bribe officials. He would regularly go to sleep listening to gunshots from rival gangs fighting over territory the block over from his house. It was completely unbridled anarchy.

I cannot even truly imagine living in such an environment, and I have lived my entire life in one of the most dangerous cities in the United States. All of that changed this year with President Bukele's declaration of martial law and an all-out war on the gangs of the country. Almost 60,000 gang members have been arrested during the course of the year, and the results have been pronounced.

The murder rate has plummeted, people are going out at night where before most people would not consider that a risk worth taking and tourism is growing. I am no stranger to living places where you have to keep your head on a swivel and pay attention to your surroundings, but not even for an instant in my week there did I feel like there was even a slight chance of something bad happening. As an outsider, it felt perfectly safe to me, and the man I met who has lived there for a decade described the El Salvador of today as an entirely different country compared to the one he moved to 10 years ago.

Have there been cases of false arrests? Yes. Is there an existential issue in sweeping aside due process to deal with the problem of violence in the country? Yes. But what would be the alternative solution anyone else would offer?

It was a common occurrence for people to be murdered over sums of money so small that here in the United States, many would just tell a cashier to keep it because they don't want to carry that small amount of change in their pockets. Yes, due process is a core tenant of a stable society, but isn't the ability to live without worry over being murdered for pocket change more important? I think it is very easy for people far removed from a situation to lecture those who aren't about how to handle them, to treat the situation as some intellectual exercise that should be approached with the goal of a perfect solution. But the real world doesn't work like that. Life is messy, and perfect solutions are almost never attainable.

Removing the massive gang presence in the country is a prerequisite to actually enabling economic growth. You can't have a growing economy if gangs are going to swoop in and extort money from people every day. No one from outside of the country is rationally going to want to take their money and invest it in such an environment. However imperfect the solution being implemented is right now, it is a solution, and it is showing results. NOTUS Energy from Germany stated its intent to invest $100 million in energy infrastructure in the country, specifically citing improvements in security in recent years as a factor. If Bukele and the current government continue the path they are on, it is very likely interest in similar investments will continue to grow.

Not An Intellectual Exercise

The Bitcoin Law has not led to instant prosperity in El Salvador, but it is laying the foundations of that to come. Chivo still has its issues, but given time, those can be improved and private solutions can be built and tailored to meet the needs of people in El Salvador. The use of Bitcoin hasn't exploded through the entire country, but the seeds of it have been planted. Similarly, the crackdown on gangs this year has not magically turned the economy and country around, but it has planted the seeds of something. Removing the gangs from the street has created room for that economic growth to happen where it otherwise would not have had the space. Things are moving in the right direction.

People looking in from the outside have tried to paint Bukele and his efforts as either unspeakable totalitarianism or an already-complete process of sculpting a utopian dream. In my opinion, they are neither. He is a man laying the foundations to allow Salvadorans the room and freedom to create their own economic prosperity.

Will it happen overnight? No. Is it guaranteed to have a positive outcome? No. But he is trying as best he can to clean up the mess left over from 30 years of corruption and violence after a brutal civil war. Bitcoiners need to step back and realize that this is a real country with real people and not some intellectual exercise to argue about on the internet.

Things seem to me to be moving in a positive direction, and I hope they continue to do so.

This is a guest post by Shinobi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

However, to what extent are these newly minted “wholecoiners” taking custody of their private keys? Has the recent spate of insolvency among centralized exchanges (CEX) encouraged Bitcoin enthusiasts to move their Bitcoin into cold storage, removed from third party risk?

For Checkmate, lead analyst at Glassnode, the data would point to this result. Checkmate told Cointelegraph, “Overall looks like, at least a short-term, movement towards self-custody. Partly out of concern for CEX solvency.”

“Last few weeks have been the largest monthly decline in exchange balances in history, peaking at 177.9k BTC/month in withdrawal volume.”

He also shared that withdrawals from exchanges have made new records, as users have taken thousands of Bitcoin from exchanges. The spike is shown in red on the graph.

Customers withdrawing Bitcoin from exchanges has impacted exchange supply. The number of Bitcoin available on exchanges has “fallen to its lowest % of supply (11.99%) since Dec 2017. This means pretty much every coin that flowed in over the last 12 months, has flowed out,” Checkmate observed.

Plus, according to Glassnode data, withdrawals from exchanges accounted “for ~30% of all transactions in recent weeks.” The data would suggest an overall shift to self-custody: Bitcoin is being sent to hot or cold wallets.

When Bitcoin investors "withdraw" from exchanges, it can be to an offline hardware wallet, sometimes called cold storage, or an online wallet (hot). Hardware wallets or signing devices are tools that manage a user’s cryptocurrency wallet and private keys. Popular hardware wallets include Ledger, Trezor and ColdCard; hot wallets include Blue Wallet or Exodus Wallet.

Josef Tětek, Bitcoin analyst at Trezor, one of the world’s largest hardware wallet providers has observed a considerable drive in sales in the past mont. Tětek told Cointelegraph, “We have seen a dramatic rise in interest in Trezor devices and new Trezor Suite downloads. Our sales are hitting historic highs over the past few weeks.”

“Normally, a bear market is rather a quiet period for us, so this uplift in sales only shows how big of an impact the collapses of FTX and BlockFi have on people's trust in custodian services.”

For Swiss-based Bitcoin exchange Relai, it’s a similar story; the company shared with Cointelegraph that it’s seen plenty of new users as well as increased volume since FTX shenanigans.

Imo Bábics, the Chief Marketing Officer at Relai told Cointelegraph:

"Well, we are non-custodial, to begin with. We have definitely noticed more people buying bitcoin due to the FTX crash.”

November was the best month in the Bitcoin exchange’s history. Relai added, “We know from our friends at ShiftCrypto that there's been a huge increase in demand for their BitBoxes."

ShiftCrypto is a hardware wallet provider like Trezor. The company’s social media feeds shared countless stories of users who recently became Bitcoin self-custody advocates following the FTX fiasco.

Some illiquid altcoins will have their borrow limit reduced by upwards of 99%.

On Nov. 28, users of decentralized finance, or DeFi, lending platform Compound Finance passed a proposal to impose restrictions on the maximum borrowing of 10 tokens on the protocol. The proposal was put forth by financial modeling firm Gauntlet and passed with a majority "Yes," although total turnout amounted to less than 7% of the COMP tokens in circulation.

Most notably, tokens such as Uniswap (UNI) and COMP had their borrow limits slashed from 11,250,000 and 150,000 to 550,000 and 18,000, respectively. Other less liquid altcoins on Compound, such as year.finance (YFI), had its borrow cap reduced from 1,500 to just 20. Coins such as wrapped Bitcoin (WBTC), which previously had no borrow limit on Compound, have been slapped with a ceiling of 1,250 on maximum borrow.

Proposal 135 has passed with quorum. ✅

Proposal 135 sets borrow caps for ten Compound v2 markets.

According to Gauntlet, the proposal would prevent "insolvency risk from liquidation cascades," "price manipulation Mango squeeze exploits," "risk of high utilization," and "risk from shorting assets from a short position on Compound of significant size relative to the circulating supply of the asset." Although the related incident was not directly referenced, Gauntlet also conducted modeling and risk assessment for DeFi lending protocol Aave.

On Nov. 22, it was uncovered that Mango Markets hacker Avraham Eisenberg attempted to exploit the protocol by shorting high amounts of Curve (CRV), which was an illiquid token on Aave at the time, and forcing the protocol to liquidate the position at a loss due to significant slippage. However, it turned out that the slippage was far less than expected, resulting in an estimated $10 million loss after a CRV short squeeze.

Gauntlet then proposed to freeze a series of tokens on Aave V2 that may be at risk of an exploit due to lack of liquidity. Currently, the Compound Finance protocol has $654.7 million in total borrowings collateralized by $2.146 billion worth of assets.

Staking infrastructure firm Kiln has closed a $17.8 million fundraising round led by the likes of Consensys, GSR and Kraken Ventures.

Staking technology provider Kiln has closed out a $17.8 million fundraising round featuring the likes of Consensys and Kraken Ventures. The company is eyeing ‘exponential’ growth in demand for ETH staking services from institutional clients in the future.

Kiln is a software-as-a-service provider focused on enterprise-grade staking solutions across 16 different proof-of-stake blockchain protocols. Its infrastructure enables users to stake on-chain while maintaining asset custody on separate solutions as well as cloud platforms and validator clients.

An announcement shared with Cointelegraph outlined growing institutionalization of cryptocurrency staking as a trend in the market. According to Kiln, this is driving the need for ‘validator-agnostic APIs and services’ to allow for multi-provider staking.

Cointelegraph spoke to Kiln co-founder and CEO Laszlo Szabo to unpack the need for multi-faceted staking services. Major exchanges and service providers like Coinbase, Ledger and Binance are serving an increasingly institutionalized staking market according to Szabo and need to interact with multiple staking providers to spread operational risk:

“The legacy solution is to manage relationships with staking providers independently, leaving the product and engineering teams of the leading companies with the task of integrating different staking providers into their workflows.”

Integrating new protocols for staking now requires custom staking and unstaking transactions for each individual protocol format, as well as running data rewards collection infrastructure and integrating custom custodian APIs.

This is a primary reason for Kiln creating a suite of products enabling wallets, custodians, and exchanges to handle multi-provider staking.

Ethereum’s recent transition to proof-of-stake (PoS) consensus also leads Sazbo to believe that demand for ETH staking will ‘grow exponentially’. His firm cited data from other PoS protocols which see between 50-80 percent of assets staked, in comparison to the 12.5% of ETH’s total supply currently staked in the Beacon chain contract.

Kiln already serves institutional clients including Ledger, Binance US and GSR. It intends to go to market with these firms with a focus on institutional segments including funds and banks.

Szabo also told Cointelegraph that the firm is in discussions with leading traditional financial institutions which are preparing comprehensive crypto-related products and exploring staking:

“They are past the discovery stage already and making significant progress even though processes are long with this kind of player.”

Ethereum’s recent transition to proof-of-stake (PoS) consensus has also driven the company's belief that demand for ETH staking will ‘grow exponentially’. The firm cited data from other PoS protocols which see between 50-80 percent of assets staked, in comparison to the 12.5% of ETH’s total supply currently staked in the Beacon chain contract.

Staking Ethereum is now an integral part of how the PoS smart contract blockchain operates on a daily basis. There are a number of staking options available to prospective users, but a full 32 ETH is required to become a validator of the network and provide participation rewards.

Everyday users looking to stake a smaller amount of ETH are able to participate in pooled staking or solutions offered by centralized exchanges.

Certain users have received emails detailing their new access to purchase and sell bitcoin on the Fidelity platform.

Fidelity, one of the world’s largest financial services providers, has officially started opening retail bitcoin trading accounts.

The development comes after their announcement of a wait list previously this month. According to a report by The Block, certain users, presumably those on the wait list, received an email detailing the release, which stated that “The wait is over.”

Fidelity has been active in the bitcoin industry for some time — according to the company website, it began mining bitcoin in 2014. In addition, it launched a spot bitcoin ETF in Canada in December of 2021.

The financial services giant’s interest in bitcoin has not come without criticism, having been the subject of U.S. senators’ scrutiny for its offering of a 401k plan that allows users to allocate to bitcoin.

The same criticism has resurfaced again recently, from the same group of senators, who stated in their latest letter, “Fidelity Investments has opted to expand beyond traditional finance and delve into the highly unstable and increasingly risky digital asset market.”

Despite these warnings, Fidelity appears to be diving headfirst into bitcoin, as interest in bitcoin amongst the traditional finance community continues to grow. It should be noted, the move comes at a particularly interesting time, given recent developments surrounding the collapse of FTX and the heightened attention being paid to volatility in the industry.

With industry perception perched so precariously, the actions of behemoths like Fidelity will almost certainly have ramifications for the future of bitcoin regulation.

The U.S.-based crypto exchange agreed to pay more than $362,000 as part of a deal “to settle its potential civil liability” related to violating sanctions against Iran.

The United States Treasury Department’s Office of Foreign Assets Control, or OFAC, has announced a settlement with crypto exchange Kraken for “apparent violations of sanctions against Iran.”

In a Nov. 28 announcement, OFAC said Kraken had agreed to pay more than $362,000 as part of a deal “to settle its potential civil liability” related to violating the United States’ sanctions against Iran. The U.S.-based crypto exchange will also be investing $100,000 into sanctions compliance controls as part of the agreement with Treasury.

“Due to Kraken’s failure to timely implement appropriate geolocation tools, including an automated internet protocol (IP) address blocking system, Kraken exported services to users who appeared to be in Iran when they engaged in virtual currency transactions on Kraken’s platform,” said OFAC.

In a statement to Cointelegraph, Kraken chief legal officer Marco Santori said the exchange had "voluntarily self-reported and swiftly corrected" its actions to OFAC:

"Even before entering into this resolution, Kraken had taken a series of steps to bolster our compliance measures. This includes further strengthening control systems, expanding our compliance team and enhancing training and accountability."

The United States has imposed sanctions on Iran that prohibit the export of goods or services to businesses and individuals in the country since 1979. However, Kraken had allegedly been violating these controls since 2019 by allowing a reported more than 1,500 individuals with residences in Iran to have accounts at Kraken — giving them the means to buy and sell crypto.

According to a July report from The New York Times, then CEO Jesse Powell — who in September announced he would step down — suggested he would consider breaking the law, through not specifically mentioning sanctions, if the benefits to Kraken outweighed any potential financial or legal penalties. The crypto exchange also reportedly allowed access to crypto for individuals in Syria and Cuba, countries sanctioned by the United States.

In September 2021, the U.S. Commodity Futures Trading Commission ordered Kraken to pay more than $1 million in civil monetary penalties for allegedly violating the Commodity Exchange Act by offering “margined retail commodity transactions in digital assets” to ineligible U.S. customers from June 2020 to July 2021. Kraken's incoming CEO, Dave Ripley, said in September he did not see a reason to register with the Securities and Exchange Commission as "there are not any tokens out there that are securities that we’re interested in listing."

Ethereum bull Anthony Sassano and Gnosis co-founder Martin Köppelmann were among those explaining later that the Wrapped Ethereum (wETH) FUD was part of an inside joke.

An inside joke about the “insolvency” of Wrapped Ethereum (wETH) over the weekend has forced influencers to explain it was just a “shitpost” after members of the community took it as real.

The wETH insolvency FUD (fear, uncertainty and doubt) seemingly began to make the rounds on Nov. 26, with false rumors alleging that wETH isn’t backed 1:1 by Ether (ETH) and is insolvent.

Blockchain developer and contributor to the ERC-721A token standard “cygaar” was one of the first to spread the joke, before confirming in a subsequent post that it was in fact a “shitpost” to see who was reading his content.

This is really a test to see who’s been reading my content.

In fact, only a day before, cygaar tweeted that “WETH cannot ever go insolvent” and that “WETH will always be swappable 1:1 with ETH.”

Ethereum bull and host of The Daily Gwei Anthony Sassano also joined in on the wETH joke with his own parody post on Nov. 27, but had to clarify later that the initial post was “shitpost/ meme” after reading the replies.

Reading the replies I feel like I should clarify

This is a shitpost/meme - there is nothing wrong with WETH and you can always redeem 1 ETH for 1 WETH

Though if you don't believe me I'll buy all of your WETH right now for 0.3 ETH

Gnosis co-founder Martin Köppelmann was another one to get in on the joke, claiming in a Nov. 27 Tweet to his 38,800 Twitter followers that wETH is no longer fully backed by ETH and that “we might see a bank run on redeeming WETH soon.”

Hours later, he said he hoped the joke “did not cause too much confusion,” linking to a thread that explained the joke for those who weren't in the know.

I hope this joke did not caused too much confusion. If you need more context find it here:https://t.co/KDN3NvdO2z

Speaking to Cointelegraph, Markus Thielen, the head of research at crypto financial services platform Matrixport has also confirmed that there is little to no truth to the WETH “shitposts.”

wETH’s logic is automated by smart contracts and it isn’t controlled by a centralized entity, he explained:

“I am not too concerned about WETH as it's a smart contract and not stored by a centralized exchange. Since the smart contract is open source, it can be checked for bugs or flaws.”

wETH was introduced as an ERC-20 token on the Ethereum network for this reason, as ETH follows different rules and thus cannot be directly traded with ERC-20 tokens.

Despite the lighthearted humor behind the jokes, “Dankrad Feist” suggested to his 15,500 Twitter followers in a Nov. 27 Tweet that the comments should be marked “more clearly as jokes” as it “may not be obvious to outsiders.”

A lot of people making jokes about WETH.

Please be aware it may not be obvious to outsiders that it's completely different from bridged assets and there is literally almost zero risk. I think it would be better to mark these more clearly as jokes.

Ripple’s APAC policy director said the collapse of FTX is exactly why crypto needs to move away from "hype cycles" and towards "real utility."

Ripple’s APAC Policy Director has described the fall of FTX as “incredibly damaging” for the crypto space, but says the industry should stand the test of time if its focus shifts towards building “real utility.”

In a statement sent to Cointelegraph, Ripple’s APAC policy lead Rahul Advani said he expects the FTX saga to lead to greater scrutiny on crypto regulations, while governments will re-evaluate “their stance towards crypto and blockchain technology,” adding:

“The collapse of FTX is incredibly damaging for the crypto space and once again underscores the need for greater regulatory clarity.”

Advani argued that the industry will need forward-looking and “flexible” regulations to boost confidence in the crypto sector while protecting consumers.

“[These regulations] must include robust measures for consumer protection but also recognize the different risks posed by business-facing crypto companies.”

“What we don't want to see is a knee-jerk response that could stifle innovation within the sector,” he added.

The Australian government is doubling down on its commitment to a crypto regulatory framework and the International Monetary Fund (IMF) called for more regulation in Africa’s crypto markets, one of the fastest-growing in the world.

Meanwhile, United States Commodity Futures Trading Commission (CFTC) commissioner Summer Mersinger said on Nov. 18 that the time to act on crypto regulation may have arrived, prompting experts to warn that crypto is in the crosshairs of U.S. lawmakers.

Advani however noted that a “one size fits all” approach to regulation “will not work” due to differing risk profiles presented by crypto companies. He instead advocated for a “risk-based approach” to regulating the industry.

He added that risks posed by crypto businesses include requirements on conduct, like segregating business accounts, disclosing conflicts of interest, and providing “retail investor safeguards.”

The EU moved in the right direction by passing a law requiring influencers to disclose the risks associated with crypto. More countries should follow their lead.

However, the crypto space is notoriously fickle, and the collapse of once-established companies such as Celsius and FTX are stark examples of how people can lose billions of dollars in crypto assets almost overnight.

For this reason, celebrity influencers should be thoroughly educated on a crypto product before promoting it. With so much at stake, this is a point that shouldn’t be overlooked by anyone in the industry.

Because of these huge risks, regulators are now asking questions regarding the ethics of celebrities using their considerable pull to draw people into crypto. And they’re not stopping at that; more jurisdictions are imposing stringent conditions for celebrities to pawn crypto products to the masses.

1/ Let’s review all the direct scams Bitboy has worked with in the past. Just in case you forgot here is the flyer with how much he charges.

I received this a while back by posing as a project interested in a promotion. pic.twitter.com/FkC9HUDGsc

For example, in the European Union, a new set of regulations known as MiCA laws will require crypto influencers to fully disclose the financial risks associated with the products they’re advertising.

Singapore is instituting even more stringent measures. The city-state will only allow crypto companies to advertise their products on their own platforms while completely barring influencers from promoting any crypto asset on social media.

What about tech entrepreneurs boosting crypto on social media?

While restricting or banning celebrities and social media influencers from pushing crypto might be commendable, another question remains unanswered. What should be done about billionaire entrepreneurs whose words have the power to influence the trajectory of crypto?

Twitter’s new owner, Elon Musk, is a known crypto proponent and a big Dogecoin (DOGE) fan. As an example of his massive influence in the crypto space, on Tuesday, April 25, just hours after his intention to buy Twitter became public, the memecoin’s price jumped by nearly 23% to $0.1677. That price was the highest it had been since January 14, when it traded at $0.2032.

And that wasn’t the only time: Several of Musk’s DOGE-related posts and comments from the past year also caused the cryptocurrency’s price to either rise or fall, depending on the sentiment Musk was sharing.

Binance CEO Changpeng Zhao, better known as CZ, is another influential voice in crypto. A casual tweet from him announcing his company was creating an industry recovery fund to help ameliorate the adverse effects of FTX’s collapse caused a surge in the price of Bitcoin (BTC) and the broader crypto market. While CZ didn’t specify the projects that the fund would be propping, or when it would become active, the news still caused BTC prices to shoot to almost $17,000.

We must consider the power of such individuals as far as influencing what we buy or sell is concerned. Regulators cannot treat the likes of Musk and CZ like ordinary people. Their words hold too much weight, especially for an industry as volatile as crypto.

Some have suggested that a Twitter spat between CZ and former FTX CEO Sam Bankman-Fried could have been the spark that caused the fire that burned FTX to the ground. These people cannot use their words so frivolously, especially not on social media.

And, while CZ has since refuted the claims that he shorted the FTX token, can we trust this to be true? After all, Binance stood to gain the most from FTX’s collapse as it now becomes the biggest crypto exchange in the world.

This might come off as controversial, but there might be a case for the likes of Musk and CZ to have their activities regulated too. After all, their voices have a significant influence in the crypto space. A whimsical social media post from someone in their rarified position can create significant upheaval in the crypto market.

Sadly, such regulation might feel like an infringement on their freedoms. Therefore, the best solution, in my opinion, would be for them to exercise greater caution in their utterances. With great power comes great responsibility, and people like them should lead by example by watching what they say. It would be unfortunate if it takes regulation to make them do so.

Benefits and drawbacks of celebrity crypto promotions

We’ve seen how Kim Kardashian and Floyd Mayweather faced legal action for unlawfully promoting crypto tokens. New Yorker Ryan Huegerich sued Mayweather, accusing the boxer of misleading investors while promoting the EMax token. The Securities and Exchange Commission, meanwhile, levied a fine on Kardashian.

The biggest problem with using celebrities to advertise crypto? While they usually command huge and eager followings, their audiences, more often than not, have little, if any, knowledge of crypto. Additionally, celebrities often have no idea about the risks associated with the products they’re promoting.

Of course, the upside of celebrity influencers endorsing crypto is the inevitable buzz they create and the vast network of influence they command. Kardashian, for example, has more than 250 million followers on Instagram. Additionally, these followers are usually hard-wired to trust the opinions of celebrities, however uneducated they might sound.

But, celebrities are also prisoners of the court of public opinion. Any PR gaffe on their part could easily crash and burn a crypto project.

And did I mention how expensive celebrities can be? Reports indicate that a promotional post on Kim Kardashian’s Instagram page will set you back anywhere between $300,000 and $1 million.

Regulations will undoubtedly help to protect us against lousy crypto decisions, but our best defense is a clear eye and lots of research. Nothing beats digging up as much information as possible about a project before putting your money into it.

Crypto winter has wrought untold havoc on investments, and it’s been exacerbated by the careless actions of some major players in the industry. The fall of companies such as FTX, Voyager, 3AC, Terra, Celsius and BlockFi only strengthen calls for the regulation of crypto.

Amid the drama, the role of celebrity endorsers should not be overlooked. As an industry, we need to find ways to ethically leverage celebrities’ popularity to promote our products.

In addition to working with the laws being put in place, I think it would be best if crypto projects thoroughly educated potential celebrity advertisers on the benefits and risks of their products. This way, influencers will be better placed to give a truer picture of what they’re selling rather than just settling for a big paycheck. I believe a little honesty will go a long way in repairing crypto’s tattered reputation.

Anastasia Kor is the chief marketing officer and a board member of crypto firm Choise.com. Before joining the company, she received degrees in economics and management from Gubkin State University of Oil and Gas, in addition to a master’s degree in marketing. She previously worked as a marketing manager for CINDX Platform.

The author, who disclosed their identity to Cointelegraph, used a pseudonym for this article. This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Famous people often have a tremendous influence on the attitudes we adopt and the decisions we make. For this reason, the crypto industry has increasingly leveraged such individuals to promote their products.

The collapse of FTX and other centralized platforms in 2022 has pushed investors toward noncustodial platforms.

The collapse of the now-bankrupt cryptocurrency exchange FTX has raised many concerns over unregulated centralized platforms.

Investors are now coming to question how safe it is to keep one’s funds on these exchanges and have voiced grave concerns about centralized decision-making without any checks.

FTX held one billion in a customer’s fund and was found to be using the customer-deposited crypto assets to mitigate its own business losses.

Furthermore, a recent report suggests that the downfall of numerous crypto exchanges over the last decade has permanently taken 1.2 million Bitcoin (BTC) — almost 6% of all Bitcoin — out of circulation.

The revelation of unethical practices by FTX in its bankruptcy filing has set a panic among investors who are already losing trust in these centralized trading firms. Exchange outflows hit historic highs of 106,000 BTC per month in the wake of the FTX fiasco and the loss of trust in centralized exchanges (CEXs) has pushed investors toward self-custody and decentralized finance (DeFi) platforms.

Users have pulled money from crypto exchanges and turned to noncustodial options to trade funds. Uniswap, one of the largest decentralized exchanges (DEX) in the ecosystem registered a significant spike in trading volume on Nov. 11, the day FTX filed for bankruptcy.

With FTX’s implosion acting as a catalyst, DEX trading has seen a notable increase in volume. Just last week, Uniswap registered over a billion dollars in 24-hour trading volume, much higher than many centralized exchanges in the same time frame.

Aishwary Gupta, DeFi chief of staff at Polygon, told Cointelegraph that the failure of centralized entities like FTX has definitely reminded users about the importance of DeFi:

“DeFi-centric platforms simply cannot fall victim to shady business practices because ‘code is law’ for them. Clearly, users realize it as well. In the wake of the FTX implosion, Uniswap flipped Coinbase to become the second-largest platform for trading Ethereum after Binance. As decentralized platforms are run by auditable and transparent smart contracts instead of people, there is simply no way for corruption or mismanagement to enter the equation.”

According to data from Token Terminal, the daily trading volume of perpetual exchanges reached $5 billion, which is the highest daily trading volume since the Terra meltdown in May 2022.

Cointelegraph reached out to PalmSwap, a decentralized perpetual exchange, to understand investor behavior in the wake of the FTX crisis and how it has impacted their platform in particular. Bernd Stöckl, chief product officer and co-founder of Palmswap, told Cointelegraph that the exchange has seen a significant bump in trading volumes.

“The usage of DeFi will surely rise thanks to the FTX downfall. It is said that Crypto.com, Gate.io, Gemini and some other centralized exchanges are in hot waters,” he said, adding, “With so many CEXs falling, trust in custodial wallets is very low and the advantages of DeFi will surely be adopted by more users.”

Elie Azzi, co-founder and DeFi infrastructure provider VALK, believes the increase in DEX volumes could be the beginning of a longer-term trend, given a general reluctance from traders to trust CEXs with their assets. He told Cointelegraph:

“DEXs are innovating at a much faster rate than their counterparts, with execution and settlement times becoming almost instantaneous on certain chains. The trend is that DEXs are developing the usability and UI of CEXs, whilst improving on the logic in the back end. Combined with the unique features that DEXs bring, including self-custody, the ability to trade from one’s own wallet and retain control of private keys.”

He added that CEX platforms might see more stringent controls and transparency initiatives, but this “transparency would exist prima facie in full DeFi. Rather, no one would need to trust CEXs with assets, and any activity, be it trading, liquidity provision or else would be recorded in real-time on-chain.”

DeFi’s struggle with targeted hacks

While DeFi protocols have seen a significant bump in the aftermath of centralized exchange failures, the nascent ecosystem itself has been a prime target for hackers in 2022.

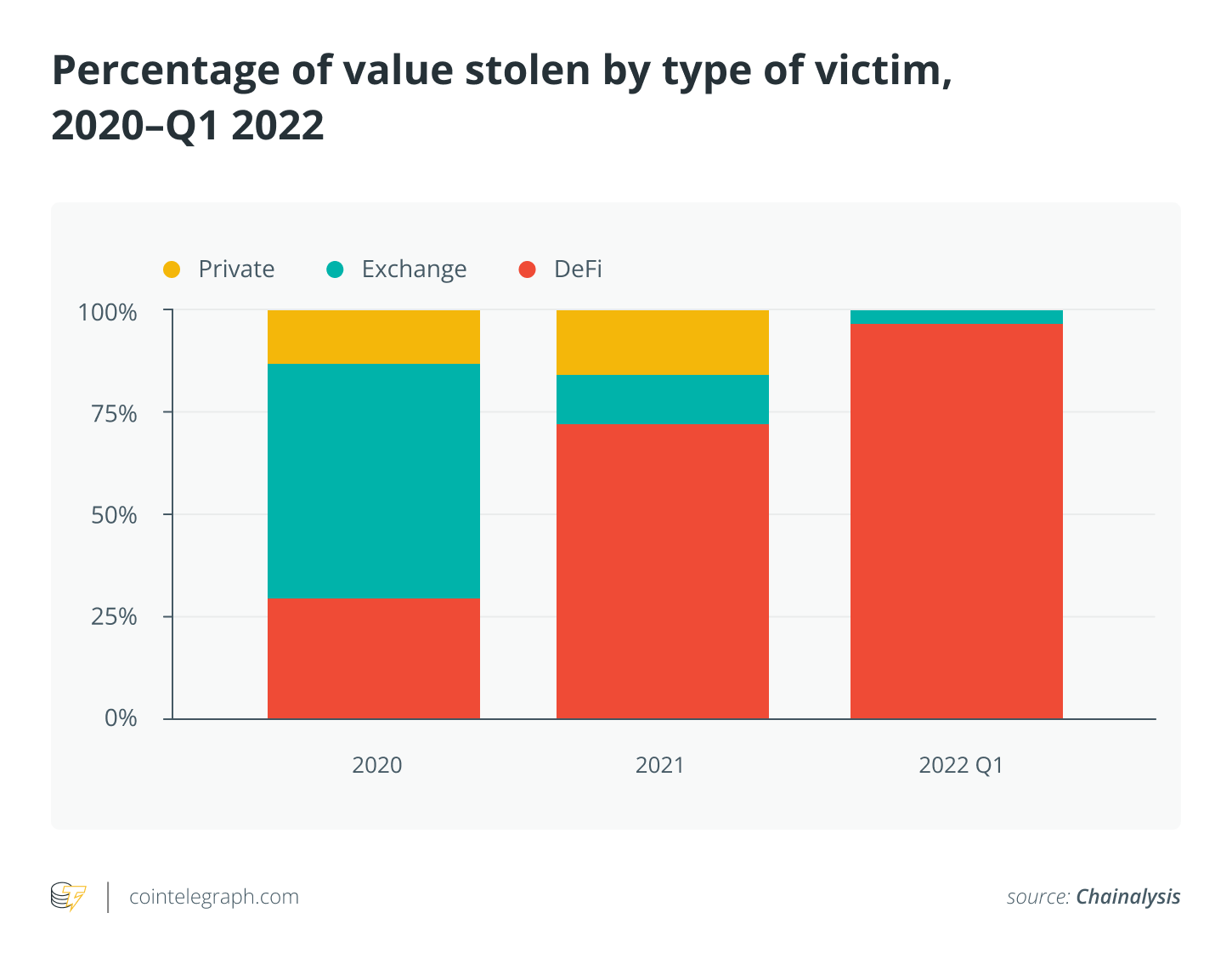

According to data from crypto analytics group Chainalysis, nearly 97% of all cryptocurrency stolen in the first three months of 2022 has been taken from DeFi protocols, up from 72% in 2021 and just 30% in 2020.

A majority of the hacks in the DeFi ecosystem have occurred on cross-chain bridges, which Jordan Kruger, CEO and co-founder at DeFi staking protocol Vesper Finance, believes shouldn’t be considered as DeFi exploits.

“A substantial proportion of those exploits (approx. $3 billion this year) have been bridge attacks. Bridges aren’t ‘DeFi’ so much as infrastructure. CEX losses dwarf this number by an order of magnitude. That said, DeFi will improve and become more secure faster than its centralized counterparts because of its ability to iterate faster. This is similar to the way Linux greatly benefitted from an open-source approach and has achieved a strong reputation for security and phenomenal adoption,” she told Cointelegraph.

DeFi is built on the ethos of true decentralization and the decision-making process is often automated via the use of smart contracts. While DeFi does try to eliminate human intervention, vulnerabilities still crop up via different mediums, be it poor coding of smart contracts or breaches of sensitive data.

Lang Mei, CEO of AirDAO, told Cointelegraph that nascent DeFi tech is prone to some bugs and issues but one must remember that the majority of hacks “have been related to either lending or cross-chain bridging, it can be immensely challenging to prevent vulnerabilities in technology which is both radically new and often has a highly-accelerated development schedule due to competition.”

He suggested additional measures that can be taken by developers to minimize the likelihood of exploitable code in their decentralized apps such as “White hat hacking, bug bounty programs, and testnet incentivization are all valuable tools to help identify and correct mistakes. They can also be used to attract and engage users, so it’s essentially a win-win from a team perspective. Decentralization of governance power is also important through the distribution of token supply and safeguards such as multi-signature wallets.”

Till Wendler, co-founder of community-owned DApp ecosystem Peaq, told Cointelegraph that it’s hard to eliminate human-related flaws in smart contacts and design.

“Most thorough smart contract security audit only gets you so far — some exploits result from the way smart contracts interact between themselves in the wider ecosystem, not just from their intrinsic design flaws,” he said, stating, “That said, the DeFi space is definitely now in a better shape than it used to be, and it’s working out its own best security practices on the go, growing more and more reliable by the hour."

Mitchell Amador, CEO at bug bounty protocol Immunefi, told Cointelegraph that DeFi can take help from progression in the security department:

“There’s a huge explosion of security tech being quietly built in the background to tackle the security problem from all angles.”

“Over time, given innovations in UX and security as well as DeFi’s inherent features of transparency, DeFi could permanently overtake centralized platforms, but this dynamic also depends on the wild card of regulations," Amador added.

The collapse of centralized platforms in 2022 and the subsequent rise of noncustodial and DeFi services in its wake is surely a sign of changing times. However, according to many in the crypto space, the most crucial factor in the FTX saga was a lack of understanding and due diligence from the crypto investors.

Myriad crypto pundits have been advocating for self-custody and the use of the decentralized platform for quite some time now. Barney Chambers, the co-founder of the Umbria Network, told Cointelegraph:

“The cryptocurrency space continues to be the wild, wild west of finance. Here are a few pointers to ensure funds are safe: Never connect your wallet to a website you don’t trust, hold your keys in a trusted place such as a hardware wallet, never trust anonymous strangers on the internet when asking for help, and always [do your own research]!”

At present, the only way investors can ensure that their funds are protected is to demand the parties they are investing in to provide transparent and clear information on all accounting and rely on noncustodial solutions in terms of both wallets and trading venues.

Darren Mayberry, ecosystem head at decentralized operating protocol dappOS, told Cointelegraph that noncustodial services should be the way forward for investors.

“Accountability and audits should be standard procedures for all investors, due diligence is a natural part of business, as is fact-checking and investigation. As for non-custodial wallets — they are the most reliable form of storage that transfers liability solely onto their owner and thus negates the possibility of counterparty risks,” he explained.

DeFi platforms might have their own set of vulnerabilities and risks, but industry observers believe that proper due diligence and reducing human error could make the nascent ecosystem of DEX platforms a go-to option over CEX platforms.